Premier Basement Remodeling in Ames for Custom Living Space

Home |

2026-03-13 12:09:19

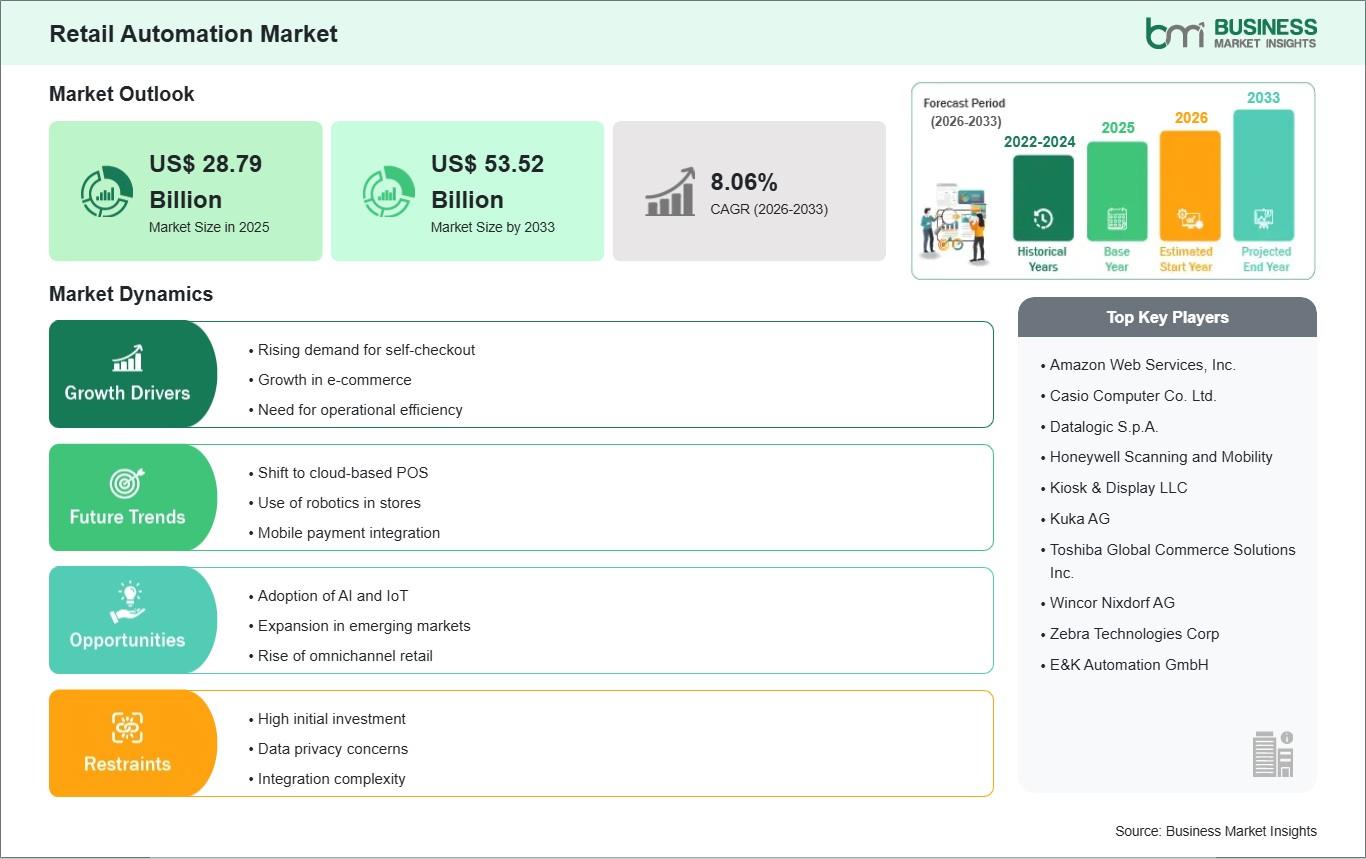

The Retail Automation Market is experiencing an unprecedented phase of growth, catalyzed by the rapid digitization of the global retail ecosystem, escalating labor operational costs, and an intense shift toward seamless, omnichannel customer experiences. By replacing manual, repetitive front-end and back-end retail operations with intelligent hardware and software systems, retail automation enables merchants to optimize inventory accuracy, streamline checkout processes, and significantly lower overhead costs while meeting the evolving demands of tech-savvy consumers.

Retail automation encompasses a broad matrix of technological solutions designed to digitize, accelerate, and manage commercial operations without requiring continuous human intervention. Historically limited to baseline electronic cash registers, modern retail automation spans from customer-facing interactive hardware to complex warehouse robotic picking machinery. In front-end brick-and-mortar settings, automation focuses primarily on removing transactional friction, optimizing shelf-space visibility, and reducing checkout queues.

In the back-end and warehouse sectors, retail automation bridges the gap between physical supply chains and digital e-commerce systems. Automated guided vehicles (AGVs), sorting conveyors, and automated storage and retrieval systems (AS/RS) allow retailers to handle massive volumes of inventory with minimal error margins. These interconnected technologies generate vast streams of behavioral and operational data, providing management teams with real-time insight into product velocity and consumer buying habits.

The primary economic driver for retail automation is the rising cost of human labor, combined with chronic workforce shortages across the service sector. Retailers face rising minimum wage laws and high employee turnover rates, forcing corporate groups to substitute flexible automated systems for manual checkout and inventory restocking workflows.

Modern consumers expect immediate, frictionless transactions mirroring their digital e-commerce experiences. Self-checkout kiosks, contactless tap-to-pay terminals, and computer vision-based "just walk out" shopping models fulfill this consumer expectation, eliminating front-end bottleneck delays and maximizing per-store customer throughput.

In an environment of fluctuating inflation and aggressive digital competitor pricing, manual paper price tag updates are highly inefficient. Automated ESL networks allow grocery and department store managers to implement dynamic pricing strategies across thousands of products instantly via centralized software, eliminating pricing discrepancies and saving substantial labor hours.

The convergence of physical shopping with online ordering (BOPIS—Buy Online, Pick Up In-Store) has forced a reconfiguration of back-end retail space. Retailers are deploying hyper-localized automated micro-fulfillment systems within backrooms to pick, sort, and pack online orders rapidly, maximizing urban real estate efficiency.

| Region / Territory | Market Dynamic & Development Landscape |

|---|---|

| North America | North America commands the largest share of the global revenue footprint, driven by a highly consolidated retail landscape, widespread corporate deployment of smart self-checkout counters, major investments in automated e-commerce dark stores, and the presence of dominant global retail tech developers. |

| Europe | Europe represents a highly mature and structured automation landscape. Growth is sustained by strong compliance standards regarding operational data protection, combined with high domestic labor costs that heavily incentivize grocery chains and hypermarket networks to implement extensive RFID and ESL tracking systems. |

| Asia-Pacific | Asia-Pacific stands out as the fastest-accelerating geographic sector. Rapidly expanding urban populations, major retail modernizations across China, India, and Southeast Asia, widespread smartphone-based digital payment integrations, and aggressive state-backed smart retail expansions are driving massive system demand. |

| Middle East & Africa | The MEA region is experiencing targeted infrastructure expansion, predominantly led by the GCC states. Mega-investments in ultra-modern retail complexes, smart city pilot programs, and high consumer affinity for premium digital luxury experiences are driving the deployment of interactive customer kiosks. |

The global retail automation market features a highly competitive and technically diverse landscape, defined by a mix of legacy hardware providers, enterprise software giants, and niche artificial intelligence developers.

Leading industry market participants focus heavily on developing software-as-a-service (SaaS) cloud platforms that unify edge-device hardware data, investing in advanced computer vision model training, and expanding strategic partnerships with major global retail conglomerates to deliver customized, scalable store-wide automation conversions.

The cutting edge of in-store innovation centers on the integration of computer vision and deep learning AI frameworks. Next-generation self-checkout terminals utilize intelligent optical cameras to automatically identify loose produce items without requiring manual barcode navigation, reducing operational checkout errors and dramatically decreasing transaction processing times.

Concurrently, autonomous shelf-auditing inventory robots are shifting out of pilot phases and onto active sales floors. Equipped with high-definition 3D mapping and RFID sensors, these mobile units navigate store aisles during off-peak hours to automatically flag misplaced products, verify price compliance on ESL tags, and document out-of-stock items, feeding real-time procurement alerts directly into automated backend supply chain systems.

The forward trajectory for the retail automation market remains highly dynamic, anchored by the evolution of hyper-personalized autonomous retail environments. The industry is moving toward a standard deployment of smart shopping carts that leverage integrated scale sensors and barcode scanners, allowing consumers to scan and pay for items directly inside their cart, bypassing physical checkout lanes entirely.

As micro-fulfillment networks continue to expand closer to urban consumer hubs, the reliance on automated dark stores—retail footprints entirely closed to the public and optimized exclusively for robotic order packing—will expand significantly. Suppliers that focus on providing highly interoperable, energy-efficient, and easily maintainable automation hardware will secure lasting supplier agreements with leading multinational grocery and retail conglomerates globally.

In-store front-end automation is predominantly driven by interactive self-checkout screens, mobile POS payment applications, electronic shelf labels (ESLs), and computer vision cameras that track product movements to enable frictionless transactions.

ESLs replace manual paper pricing tags with digital displays connected to a centralized server. This allows retailers to implement instantaneous, real-time price changes across thousands of products, ensuring complete pricing synchronization with online channels and eliminating extensive manual labor hours.

Micro-fulfillment centers utilize localized, compact warehouse robotics within back-of-store areas to automatically pick and sort online orders. This system significantly minimizes the time required to assemble e-commerce orders, facilitating ultra-fast home deliveries or immediate curbside pickups.

While early self-checkout lines faced elevated shrink risks, modern automated systems integrate weight-sensing platforms, computer vision surveillance, and artificial intelligence models that actively flag suspicious checkout behavior or scanning errors to protect retail margins.