Stop Drowning in Deadlines — UK's Expert Essay Writers Are Here to Change the Game

Other |

2026-04-08 12:32:34

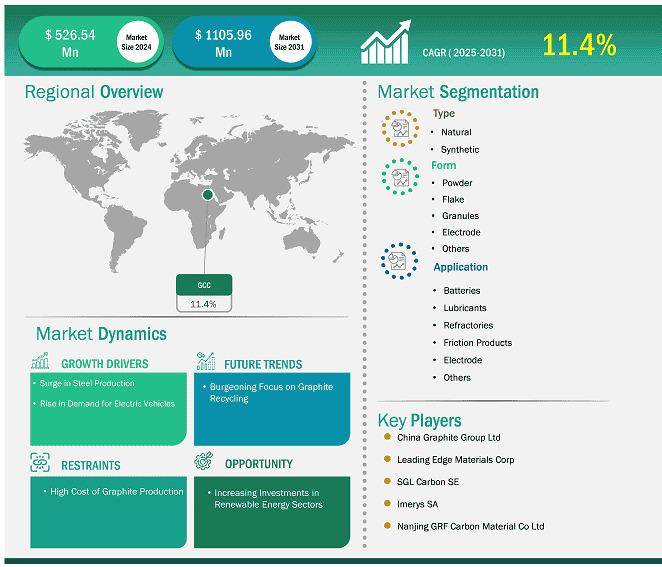

The GCC Graphite Market is witnessing notable expansion, propelled by the accelerating industrial diversification strategies across the Gulf Cooperation Council (GCC), substantial growth in the regional steel and aluminum manufacturing sectors, and emerging clean energy storage initiatives. As member states actively execute long-term strategic blueprints like Saudi Arabia's Vision 2030 and the UAE's We the UAE 2031, traditional oil-dependent economies are aggressively scaling up localized industrial supply chains, driving a robust demand for high-purity natural and synthetic graphite configurations.

Graphite is a crystalline form of carbon known for its exceptional thermal and electrical conductivity, high chemical inertness, and structural resilience at extreme temperatures. These unique physical properties make it an indispensable raw material across both heavy industrial manufacturing and high-technology clean energy applications.

Modern industrial applications seamlessly utilize both natural graphite (extracted via traditional mining) and synthetic graphite (produced from petroleum coke or coal tar pitch). While legacy metallurgy operations rely heavily on graphite for refractories and casting molds, emerging manufacturing sectors across the GCC are pivoting toward ultra-pure spherical graphite to support localized battery storage grids and modern electronic thermal management systems.

One of the primary growth drivers for the industry is the massive capital deployment toward non-oil sector development across Saudi Arabia, the UAE, Qatar, and Oman. Governments are consistently establishing heavily incentivized industrial cities, which directly accelerates the domestic consumption of metallurgical and chemical processing raw materials.

The GCC region hosts some of the world's largest and most efficient aluminum smelters and expanding steel production complexes. Because graphite serves as a core component in the electrodes, refractories, and carbon additives used throughout heavy metallurgy, sustained infrastructure spending ensures a predictable, recurring volume demand.

As the Gulf region rapidly scales up massive utility-scale solar photovoltaic (PV) complexes, the demand for robust energy storage systems (ESS) is rising. Graphite anodes are critical to the performance of high-capacity lithium-ion battery architectures, making the material central to the region’s long-term clean energy transition goals.

Several GCC nations are actively positioning themselves as emerging hubs for electric vehicle (EV) assembly and battery component processing. Strategic investments in localized manufacturing clusters create extensive downstream supply pathways for high-grade spherical and synthetic graphite variants.

| Country / Territory | Market Dynamic & Development Landscape |

|---|---|

| Saudi Arabia | The Kingdom commands a dominant position in the GCC market, sustained by its massive heavy industrial cities (Jubail and Yanbu), expanding electric arc furnace steel production, and active investments to localize EV battery and automotive ecosystems under Vision 2030. |

| United Arab Emirates | The UAE is experiencing significant expansion driven by high-capacity aluminum smelting complexes (such as EGA) and a rapid regulatory push toward clean energy technology integration, positioning Dubai and Abu Dhabi as regional hubs for advanced material trade. |

| Qatar | Qatar exhibits a steady, high-value demand profile linked to its specialized industrial manufacturing clusters, continuous construction updates for downstream chemical infrastructures, and localized metallurgical refining projects. |

| Oman | Oman is showing targeted growth, focused heavily around the Sohar and Duqm industrial free zones, where expanding steelmaking projects and maritime manufacturing supply chains create a steady consumption curve for industrial refractories. |

| Rest of GCC | Comprising Bahrain and Kuwait, this segment shows stable market operations, largely supported by established aluminum production facilities (such as Alba in Bahrain) and localized industrial maintenance requirements. |

The regional market landscape features a blend of global material suppliers, specialized chemical distributors, and international carbon product manufacturing entities establishing long-term commercial trade agreements with domestic industrial groups.

Primary market participants focus heavily on optimizing their logistics networks, securing long-term raw material off-take agreements, and delivering specialized high-density graphite grades capable of enduring the intense thermal parameters common in heavy desert industrial zones.

Material engineering and processing developments are fundamentally altering industrial consumption trends across the GCC. Advanced coating techniques for natural flake graphite are drastically improving the electrical conductivity and cyclical lifespans of battery anodes, facilitating a broader commercial acceptance of natural variants alongside historically preferred synthetic configurations.

Furthermore, local industrial hubs are evaluating next-generation ultra-high-power (UHP) synthetic graphite electrodes that maximize operational efficiency inside electric arc furnaces. These advanced material architectures lower localized power consumption metrics per ton of refined steel, helping local heavy industries manage structural overhead while working to lower their scope 1 emission values.

The forward trajectory of the GCC graphite market remains highly positive, strongly supported by the continuous regional transformation of heavy metal refining into highly automated, energy-efficient operational structures. The continuous evolution of downstream battery manufacturing plants and localized solar storage architectures ensures a predictable, expanding demand curve for high-purity graphite inputs.

As sustainability frameworks become deeply integrated into regional procurement guidelines, data verification concerning supply chain tracing will emerge as a standard mandate. Manufacturers and distributors that provide clear structural performance guarantees paired with optimized regional inventory hubs will successfully secure long-term purchase contracts with major industrial operators across the Gulf.

The market expansion is accelerated by heavy industrial diversification initiatives, expanding aluminum and steel production capacities, the scaling of regional infrastructure projects, and emerging investments in solar energy storage and EV ecosystems.

Synthetic graphite holds a dominant market footprint due to its extensive use in high-power graphite electrodes for electric arc furnace steelmaking and primary aluminum smelting operations across the region.

These national blueprints actively incentivize and fund the creation of non-oil industrial sectors, manufacturing hubs, and green energy infrastructures, which directly creates vast consumption pathways for advanced industrial minerals like graphite.

High-purity graphite is the primary material utilized to manufacture the anodes of lithium-ion batteries. These battery systems are essential for storing energy generated by the GCC's massive utility-scale solar farms and powering next-generation electric vehicles.