Job Opportunities in the USA Through Online Hiring Platforms

Other |

2026-03-17 09:22:31

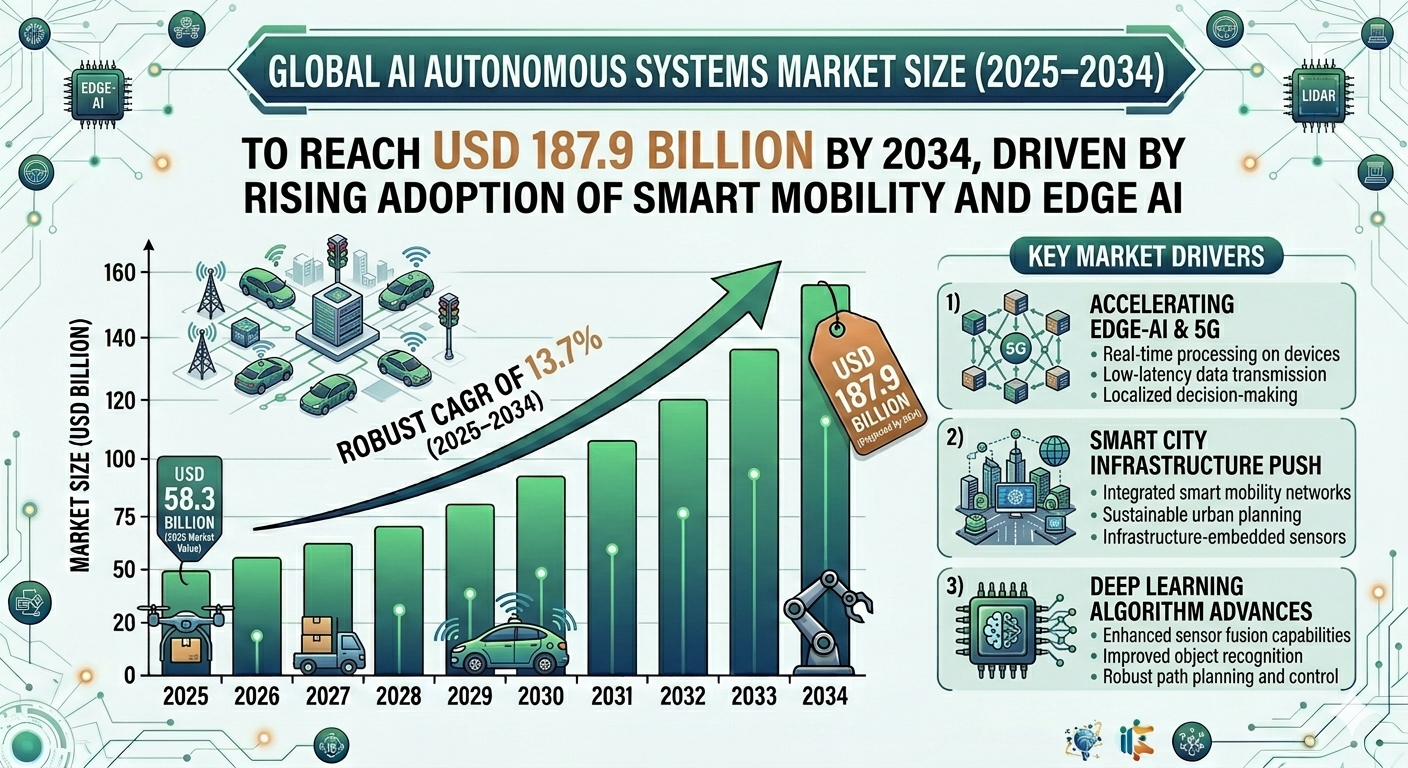

According to a new report from Intel Market Research, the global AI autonomous systems market was valued at USD 58.3 billion in 2025 and is projected to reach USD 187.9 billion by 2034, growing at a robust CAGR of 13.7 % during the forecast period (2025–2034). This expansion is driven by rapid advances in deep‑learning algorithms, the convergence of edge‑AI and 5G connectivity, and escalating investments in smart‑city infrastructure that demand highly reliable autonomous solutions across a spectrum of industries.

AI autonomous systems refer to integrated computational frameworks that empower machines, vehicles and software to perceive, decide and act without human intervention. Leveraging artificial intelligence, machine learning, and real‑time data processing, these systems span self‑driving cars, unmanned aerial vehicles (UAVs), robotic process automation (RPA), industrial robotics, and intelligent decision‑making platforms used in transportation, manufacturing, healthcare, defense, logistics and many other sectors. Core components include high‑resolution perception sensors (LiDAR, radar, cameras), AI‑driven perception and mapping algorithms, predictive analytics engines for decision‑making, and actuation modules that translate digital commands into physical motion.

📥 Download FREE Sample Report:

AI Autonomous Systems Market - View in Detailed Research Report

What is AI Autonomous Systems?

AI autonomous systems are engineered to execute complex tasks with minimal or no human supervision. By fusing sensor data with sophisticated AI models, these platforms create a dynamic representation of their operating environment, predict future states, and generate control commands in milliseconds. In the automotive arena, this translates to Level‑4 and Level‑5 self‑driving capabilities; in logistics, it enables autonomous forklifts and drone‑based parcel delivery; in healthcare, it powers surgical robots that can adapt to intra‑operative variations; and in defense, it delivers unmanned ground and aerial platforms capable of autonomous navigation in contested spaces.

This report provides a deep insight into the global AI autonomous systems market covering all its essential aspects-from a macro overview of market size and growth trends to micro details such as competitive landscape, technology road‑maps, niche applications, key drivers and challenges, SWOT analysis, and value‑chain assessment.

The analysis helps readers understand competition within the industry and formulate strategies for enhancing profitability. Moreover, it offers a structured framework for evaluating the strategic positioning of organizations, assessing partnership opportunities, and anticipating regulatory shifts. The report also focuses on the competitive landscape of the Global AI Autonomous Systems Market, introducing market‑share, performance, product positioning, and operational insights of major players. This helps industry professionals identify key competitors and understand evolving market patterns.

In short, this report is a must‑read for technology providers, automotive OEMs, logistics operators, investors, consultants, business strategists, and any stakeholder planning to foray into the AI autonomous systems market.

Key Market Drivers

1. Surge in Demand for Operational Efficiency

Enterprises across manufacturing, warehousing and transportation are confronting intense pressure to cut costs, reduce human error and improve throughput. AI‑enabled autonomy automates repetitive, high‑precision tasks, freeing skilled labor for higher‑value activities. The resulting productivity boost and lower operational expenditure are compelling reasons for rapid adoption, especially in regions where labor costs are rising.

2. Breakthroughs in Deep‑Learning and Sensor Fusion

Continuous improvements in convolutional neural networks, transformer‑based perception models and reinforcement‑learning decision engines have dramatically increased the accuracy and reliability of autonomous perception. Coupled with next‑generation sensor suites-high‑resolution LiDAR, solid‑state radar and hyperspectral cameras-these algorithms now achieve near‑human level scene understanding, unlocking use‑cases previously considered too risky.

➤ Key Insight: The synergy between 5G connectivity and edge computing is enhancing the speed and reliability of data transmission, a critical component of modern AI Autonomous Systems.

3. Expanding Smart‑City and Infrastructure Investments

Governments worldwide are channeling billions into smart‑city projects that require autonomous mobility, intelligent traffic management and automated public services. These macro‑level initiatives create a fertile ecosystem for AI autonomous platforms, providing both the physical infrastructure (connected roadways, dedicated lane markings) and the policy incentives (tax credits, regulatory sandboxes) that accelerate market penetration.

Market Challenges

Complexity in System Integration

Deploying autonomous capabilities often means retrofitting legacy equipment with modern AI hardware and software stacks. Integration challenges-such as mismatched communication protocols, disparate data formats and the need for extensive validation-can lead to prolonged implementation cycles and unanticipated costs, especially for mid‑size manufacturers with limited engineering resources.

High Cost of Development and Deployment

The development of robust AI models, acquisition of high‑precision sensors and certification of safety‑critical systems demand substantial capital outlays. Small and medium‑sized enterprises may struggle to secure the necessary financing, creating a market entry barrier that favors large, well‑capitalized players.

Reliability and Safety Concerns

Ensuring fail‑safe operation in unpredictable real‑world environments remains a paramount concern. Regulatory bodies worldwide are tightening safety standards, and any high‑profile incident can trigger public backlash and stricter oversight, slowing commercialization timelines.

Market Restraints

Regulatory and Compliance Hurdles

The AI autonomous systems market is constrained by an evolving regulatory landscape. Governments and regulatory bodies are still formulating comprehensive policies to address safety standards, liability issues, and ethical considerations for autonomous operations. The lack of clear, universal regulations often creates uncertainty for manufacturers and operators, leading to a cautious approach to deployment and slowing down the market's expansion potential.

Emerging Opportunities

Expansion in Healthcare Robotics

The healthcare sector offers immense potential for AI autonomous systems. There is a growing demand for autonomous surgical robots, intelligent diagnostic assistants and remote patient‑monitoring platforms that can operate with high precision and speed. As the global population ages, the need for efficient healthcare delivery and remote monitoring will drive significant investment in intelligent medical devices, opening new revenue streams for market participants.

Autonomous Logistics & Supply‑Chain Automation

E‑commerce growth and the push for resilient supply chains are spurring adoption of autonomous trucks, last‑mile delivery drones and warehouse robotics. These solutions reduce labor dependency, cut transit times and improve order‑fulfilment accuracy, positioning AI autonomy as a cornerstone of next‑generation logistics.

Regional Market Insights

Market Segmentation

By Application

By End User

By Distribution Channel

By Region

Competitive Landscape

The AI autonomous systems market is dominated by a handful of technology powerhouses and automotive OEMs that have integrated advanced perception, decision‑making and control algorithms into real‑world products. Waymo (Alphabet), Tesla, Cruise (General Motors), Baidu Apollo, NVIDIA, Mobileye (Intel), Aurora Innovation, Nuro, Zoox (Amazon), DJI and Boston Dynamics are among the most visible players. Their strategies range from proprietary hardware‑software stacks to open‑source platforms, extensive data‑fleet collection and strategic partnerships with cloud providers, semiconductor manufacturers and vehicle makers.

Beyond the marquee names, a vibrant ecosystem of specialized firms fuels niche innovations and regional deployments. Companies such as Mobileye focus on vision‑only ADAS and Level‑2+ solutions, while NVIDIA underpins many deployments with GPU‑accelerated AI processors. Xilinx (AMD) and IBM contribute specialized AI ASICs and edge‑computing services, respectively, enabling tighter integration of inference workloads within vehicle ECUs and industrial controllers.

List of Key AI Autonomous Systems Companies Profiled

Report Deliverables

📘 Get Full Report Here:

AI Autonomous Systems Market - View Detailed Research Report

📥 Download Sample Report: AI Autonomous Systems Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia‑Pacific: +91 9169164321

🔗 LinkedIn: Follow Us