Dubai Aesthetic Clinics with Liposuction Expertise

Health |

2026-03-05 05:54:27

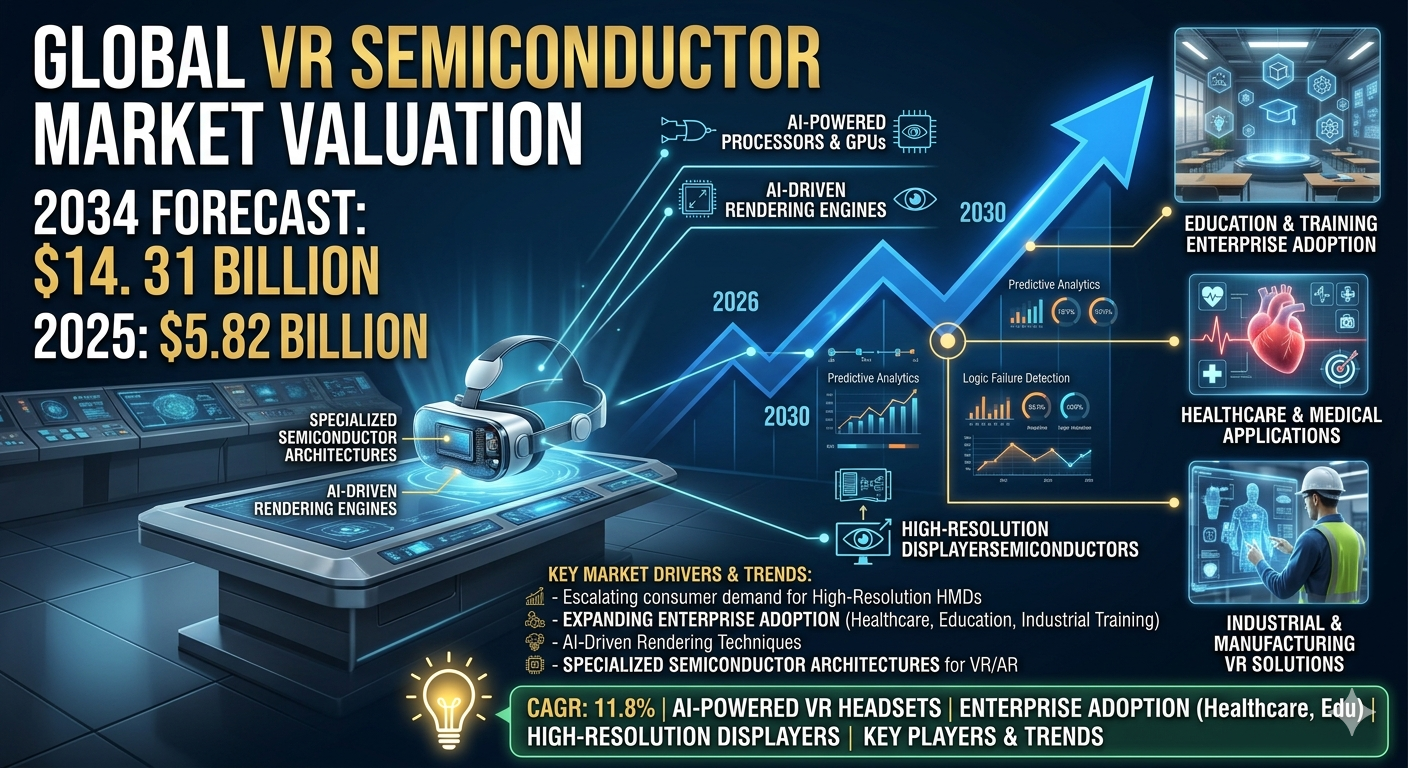

According to a new report from Intel Market Research, the global VR semiconductor market was valued at USD 5.82 billion in 2025 and is projected to reach USD 14.31 billion by 2034, exhibiting a robust CAGR of 11.8% during the forecast period (2026–2034). This growth is propelled by escalating consumer demand for high‑resolution head‑mounted displays, expanding enterprise adoption in healthcare, education, and industrial training, and rapid advances in AI‑driven rendering techniques that rely heavily on specialized semiconductor architectures.

What is VR Semiconductor?

VR semiconductors are purpose‑built integrated circuits that power immersive virtual‑reality experiences. They encompass GPUs (Graphics Processing Units), CPUs (Central Processing Units), SoCs (System‑on‑Chips), high‑bandwidth memory, and dedicated sensors. Together, these components enable ultra‑high pixel‑rates, sub‑10 ms motion‑to‑photon latency, and advanced graphics features such as ray‑tracing and foveated rendering. Unlike traditional chips that target generic computing, VR‑specific silicon is engineered for thermal efficiency, power optimisation, and deterministic performance to mitigate motion sickness and deliver seamless interaction.

This report provides a deep insight into the global VR semiconductor market covering all essential aspects-from a macro overview of market size and growth dynamics to micro‑level analysis of competitive landscape, technology roadmaps, key drivers and challenges, SWOT assessment, and value‑chain mapping. The analysis assists stakeholders in understanding competitive pressures, identifying high‑growth niches, and formulating strategies that enhance profitability across the ecosystem.

📥 Download FREE Sample Report:

VR Semiconductor Market - View in Detailed Research Report

Key Market Drivers

1. Increasing Demand for High‑Resolution VR

The proliferation of consumer‑grade headsets featuring 4K‑per‑eye displays and refresh rates above 90 Hz is compelling chip makers to deliver silicon that can handle massive pixel‑rates while preserving low latency. This demand fuels innovation in GPU bandwidth, memory architecture, and display‑driver integration.

2. Advancements in Process Technology

Sub‑10 nm nodes now enable the integration of AI accelerators directly within VR chips, improving inside‑out tracking, eye‑tracking, and real‑time rendering efficiency. The resulting reduction in bill‑of‑materials cost and shortened time‑to‑market accelerates adoption across gaming and enterprise segments.

➤ Analysts project that 2025 will see a 15 % increase in wafer shipments dedicated to VR applications, driven by these process improvements.

3. Enterprise Training & Simulation

Businesses in aerospace, automotive, and medical sectors are investing heavily in VR‑based training platforms that require high‑fidelity graphics and low‑latency sensor fusion. This creates a steady demand for rugged, performance‑centric semiconductors capable of delivering realistic haptic feedback and precise motion cues.

4. AI‑Enhanced Rendering Techniques

Techniques such as foveated rendering and ray‑tracing acceleration depend on dedicated AI cores and tensor accelerators embedded within SoCs. By off‑loading these compute‑intensive tasks, manufacturers achieve up to a 30 % reduction in overall computational load while preserving visual quality.

Market Challenges

Supply Chain Volatility

Geopolitical tensions and periodic shortages of advanced substrates have lengthened lead times for critical components. Companies are compelled to diversify sourcing strategies and increase inventory buffers to safeguard production continuity.

Thermal Management

Higher performance chips generate increased heat, posing risks to user comfort and device reliability. Innovative cooling solutions, such as vapor‑chamber designs and silicon‑on‑insulator (SOI) technologies, are being explored to address this hurdle.

Regulatory Hurdles

Emerging safety standards for electromagnetic emissions and eye‑safety add design complexity, inflating development costs and extending time‑to‑market cycles.

Market Restraints

High Capital Expenditure

Establishing fab capacity for next‑generation VR chips demands multi‑billion‑dollar investments, limiting entry to well‑funded incumbents. The need for specialised testing equipment further elongates qualification timelines.

Legacy Hardware Reluctance

Customers often hesitate to upgrade existing headset platforms, curbing short‑term demand for newer semiconductor solutions and creating a risk of inventory obsolescence for manufacturers.

Market Opportunities

Enterprise Training & Simulation

The growing adoption of VR for safety‑critical training in manufacturing, defense, and medical education presents a lucrative avenue for semiconductor providers to deliver low‑latency, high‑precision compute blocks.

Emerging Markets in Asia‑Pacific

Rapid expansion of VR‑enabled curricula in schools and vocational institutes across China, India, and Southeast Asia offers a sizable growth frontier for component suppliers seeking cost‑effective yet performant solutions.

Mixed‑Reality Convergence

The blending of AR and VR into unified mixed‑reality platforms widens the addressable market, encouraging chipmakers to develop flexible architectures that support both optical see‑through and immersive stereoscopic experiences.

Segment Analysis

|

Segment Category |

Sub‑Segments |

Key Insights |

|

By Type |

|

Analog VR SoC delivers tightly integrated analog front‑ends that reduce board complexity and power consumption, enabling higher‑precision sensor interfacing essential for ultra‑low latency head‑tracking. This form factor is preferred in compact headsets where space and thermal budgets are constrained. |

|

By Application |

|

Gaming remains the dominant application, driving ultra‑low latency and high frame‑rate requirements that push semiconductor innovation. Enterprise and healthcare use‑cases demand robust, reliable processing with extended product life cycles. |

|

By End User |

|

Professional users prioritize reliability, expanded I/O, and support for advanced sensor suites such as eye‑tracking and hand‑gesture modules. Long product life cycles and robust thermal solutions shape their component selection. |

|

By Integration Level |

|

Fully Integrated Chip is gaining traction as manufacturers seek to shrink form‑factor and improve power efficiency. Consolidating analog front‑ends, processing cores, and memory controllers onto a single die reduces inter‑connect parasitics, a critical factor for maintaining low latency in VR pipelines. |

|

By Performance Tier |

|

High‑Performance segments drive differentiation through advanced process nodes and specialized AI accelerators, enabling sophisticated rendering techniques such as foveated shading and real‑time ray tracing for premium headsets. |

Competitive Landscape

The VR semiconductor arena is anchored by a handful of dominant chipset manufacturers that combine high‑performance graphics cores with low‑latency vision processing. Key players include:

These firms benefit from extensive developer ecosystems, strong IP portfolios, and deep relationships with headset OEMs, granting them pricing power and market share advantages. Niche manufacturers contribute specialized components-such as high‑bandwidth memory, photonic interconnects, and neuromorphic accelerators-that complement the core offerings of the dominant players and foster a vibrant, innovation‑driven marketplace.

Technology & Innovation Trends

Advances in Process Technology

The market is witnessing a rapid transition to sub‑10 nm nodes, with EUV‑enabled 7 nm and 5 nm processes improving transistor switching speed while lowering power draw. Gate‑all‑around (GAA) architectures further boost drive current without increasing leakage, enabling more compute units within the limited silicon real estate of compact VR chips.

Integration of AI Accelerators

AI‑dedicated cores are increasingly embedded alongside traditional graphics pipelines to handle real‑time eye‑tracking, foveated rendering, and adaptive bitrate control. These tensor units reduce end‑to‑end latency and improve power efficiency, allowing lighter headset form factors without sacrificing performance.

Shift Toward 2.5‑Dimensional Packaging

2.5‑D interposer technologies facilitate heterogeneous integration of high‑bandwidth memory (HBM) and processing dies, shortening signal paths and improving thermal distribution. This packaging innovation supports sustained 120 Hz+ refresh rates at 4K resolution while maintaining a thermal envelope suitable for lightweight devices.

Regional Analysis

North America

The region remains the largest market for VR semiconductors, driven by a strong consumer electronics ecosystem, leadership in gaming, and substantial enterprise R&D investment. Venture‑capital‑backed VR startups accelerate adoption of next‑gen silicon, while convergence with AI and 5G fuels new use cases in training, design visualization, and remote collaboration.

Europe

Europe shows steady growth, propelled by government‑backed innovation programs, a mature gaming market, and increasing industrial adoption of VR for manufacturing and aerospace training. Regulatory frameworks supporting data privacy and safety create a stable environment for semiconductor expansion.

Asia‑Pacific

Asia‑Pacific is the fastest‑growing region, underpinned by massive consumer demand for VR gaming in China, Japan, and South Korea, as well as rising educational initiatives that incorporate VR into curricula. Local hardware manufacturers and foundries stimulate demand for domestically‑produced chips, reducing reliance on imports.

Latin America

Growth is nascent but accelerating, with improving internet penetration and falling headset prices enabling broader consumer adoption. Enterprise training in mining and oil‑&‑gas sectors is emerging as a notable driver.

Middle East & Africa

While currently modest in scale, the region is beginning to explore VR for training, medical education, and entertainment. Infrastructure challenges and lower disposable incomes temper rapid expansion, but governmental digital transformation agendas hint at future upside.

Report Deliverables

📘 Get Full Report Here:

VR Semiconductor Market - View Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us