Blood Strike Update: M82 Sniper & Peak Legend Tier

Games |

2025-09-24 01:22:49

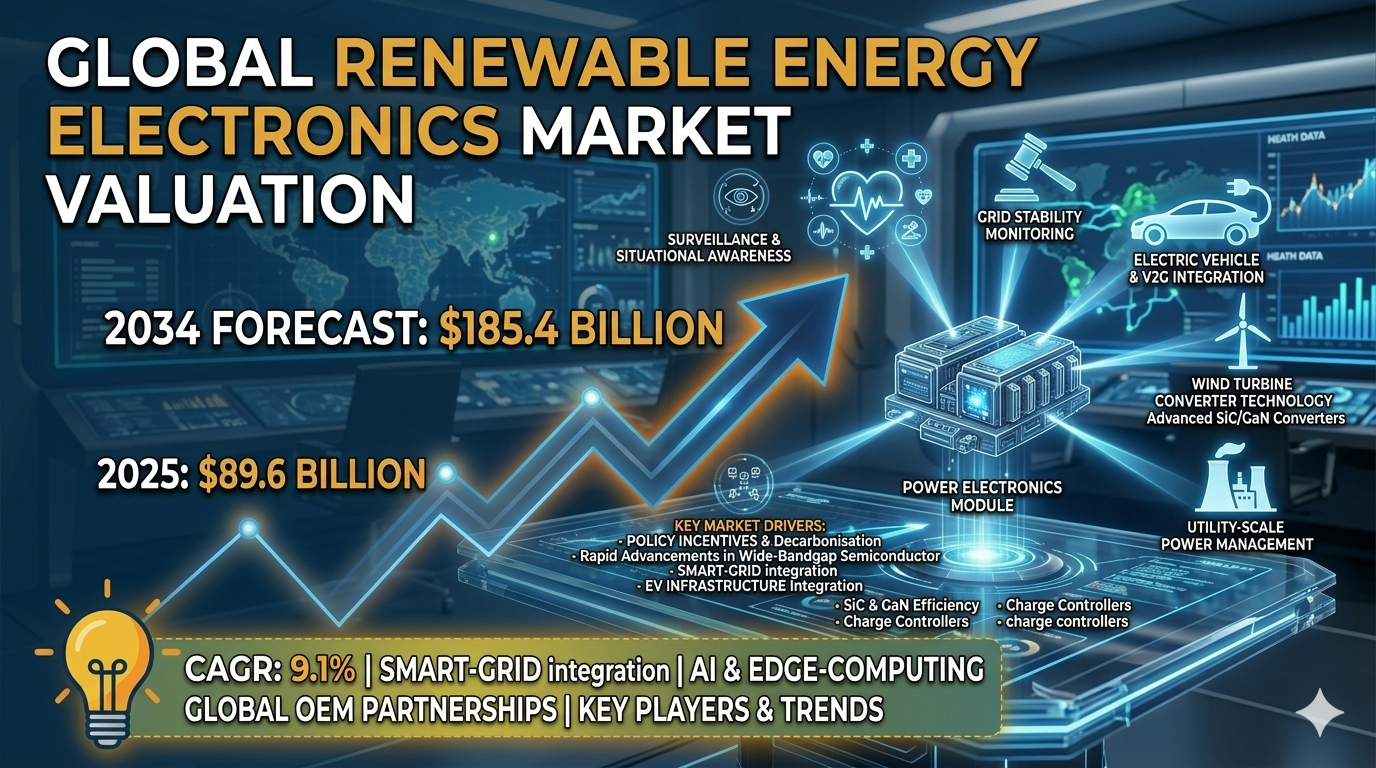

According to a new report from Intel Market Research, the global Renewable Energy Electronics market was valued at USD 89.6 billion in 2025 and is projected to reach USD 185.4 billion by 2034, exhibiting a robust CAGR of 9.1% during the forecast period (2026–2034). This growth is propelled by escalating demand for clean‑energy solutions, supportive policy frameworks, rapid advancements in wide‑bandgap semiconductor technologies, and the expanding integration of renewable energy sources with smart‑grid and electric‑vehicle infrastructures.

What is Renewable Energy Electronics?

Renewable Energy Electronics encompass advanced electronic components and systems designed to harness, convert, and manage energy from renewable sources such as solar, wind, hydro, and geothermal power. The portfolio includes power converters, inverters, charge controllers, energy storage systems (ESS), smart‑grid communication modules, and power optimisers. Innovations in wide‑bandgap semiconductors-silicon carbide (SiC) and gallium nitride (GaN)-are reshaping the industry by delivering higher power densities, lower losses, and enhanced thermal performance.

This report provides a deep insight into the global Renewable Energy Electronics market covering all essential aspects-from a macro overview of market size and growth trends to micro‑level analyses such as competitive landscape, technology roadmaps, segmentation, regional dynamics, and strategic opportunities.

📥 Download FREE Sample Report:

Renewable Energy Electronics Market - View in Detailed Research Report

📘 Get Full Report Here:

Renewable Energy Electronics Market - View Detailed Research Report

Key Market Drivers

1. Policy Incentives and Decarbonisation Targets

Robust government policies worldwide mandate lower carbon emissions and provide subsidies for solar inverters, wind turbine converters, and energy‑storage controllers. Predictable regulatory environments stimulate investments from incumbents and new entrants alike.

2. Technological Advancements and Cost Reductions

Continuous improvements in semiconductor efficiency, especially SiC and GaN devices, have reduced bill‑of‑materials costs. These advances make renewable energy systems financially viable for both commercial and residential users, accelerating market adoption.

➤ The adoption rate of smart‑grid‑compatible inverters is accelerating, driven by the need for real‑time monitoring and grid stability.

As utilities modernise the grid, demand for advanced power electronics that provide ancillary services and demand‑response capabilities continues to rise, further supporting market expansion.

Market Challenges

Regulatory Complexity and Certification Hurdles

Navigating diverse certification regimes-IEC, UL, ISO-across regions poses significant challenges for manufacturers aiming for global scale. Non‑compliance can delay product launches and increase costs.

Supply Chain Constraints

Limited availability of high‑purity silicon and rare‑earth materials for power‑electronics components can cause production bottlenecks, especially during periods of rapid market growth. Geopolitical tensions add an additional layer of uncertainty.

Market Restraints

High Initial Capital Expenditure

Although renewable energy systems deliver long‑term savings, the upfront cost of advanced power‑electronics equipment-particularly for large‑scale solar farms and offshore wind-remains a deterrent for many project developers, tempering near‑term market penetration.

Emerging Opportunities

Smart‑Grid Integration

Opportunities abound in developing interoperable electronics that support micro‑grid management, vehicle‑to‑grid (V2G) services, and AI‑driven predictive maintenance. Companies that deliver modular, software‑defined solutions are positioned to capture a sizable share of the evolving market.

Regional Market Insights

Market Segmentation

By Type

By Application

By End User

By Technology

By Region

Competitive Landscape

The Renewable Energy Electronics market is dominated by integrated power‑electronics manufacturers that supply inverters, converters, and grid‑interface solutions for solar, wind, and storage applications. Siemens Energy retains a leadership position through its extensive portfolio of grid‑forming converters and high‑voltage technology, leveraging a global service network that stabilises large‑scale projects. ABB Ltd. and Schneider Electric SE follow closely, each offering modular inverter platforms that address utility‑scale and distributed generation alike, while General Electric differentiates itself with digital‑twin analytics for predictive maintenance and optimal dispatch.

Niche yet influential players continue to shape specialised segments. SMA Solar Technology and Enphase Energy excel in residential‑solar inverter technology, with Enphase’s micro‑inverter architecture driving rapid adoption in rooftop installations. Asian incumbents such as Huawei, Sungrow Power, and Mitsubishi Electric provide cost‑competitive string inverters and storage converters that dominate emerging markets in Southeast Asia and Africa. Meanwhile, Delta Electronics and Vicor focus on high‑efficiency power‑module designs for offshore wind and electric‑vehicle charging infrastructure, underscoring the market’s diversification across both geographical and application‑specific fronts.

List of Key Renewable Energy Electronics Companies Profiled

Technology Innovation & R&D Trends

Wide‑bandgap semiconductor research remains at the core of the market’s evolution. SiC devices now achieve efficiencies above 99 % in high‑power inverters, allowing reductions in cooling infrastructure and enabling compact, high‑density converter designs for offshore wind platforms. GaN technology is gaining traction in lower‑power residential inverter applications, where its high switching speed translates into smaller footprints and lower acoustic noise.

Artificial intelligence and edge‑computing are being embedded directly into power‑electronics modules. AI‑driven control algorithms dynamically optimise pulse‑width modulation, harmonise phase‑balancing, and predict component wear, providing utilities with unprecedented visibility into system health. These capabilities are especially valuable for micro‑grid deployments where autonomous operation and rapid fault isolation are essential.

In parallel, the industry is moving toward eco‑design principles. Manufacturers are adopting recyclable aluminium casings, lead‑free solder, and modular architectures that enable end‑of‑life refurbishment. Such sustainability initiatives align with the broader ESG goals of renewable‑energy project developers and are expected to become differentiators in procurement decisions.

Future Outlook (2025‑2034)

By the end of the forecast horizon, the Renewable Energy Electronics market is anticipated to have more than doubled in size, driven by three converging forces: (1) the continued rollout of utility‑scale solar and wind farms that demand high‑efficiency, grid‑forming converters; (2) the proliferation of behind‑the‑meter storage solutions that rely on sophisticated battery‑management electronics; and (3) the maturation of smart‑grid standards that mandate interoperable, communication‑enabled power electronics.

Geographically, the Asia‑Pacific region is projected to record the fastest compound growth, buoyed by China’s ongoing megaprojects, India’s aggressive renewable targets, and Japan’s focus on offshore wind. Europe will retain the largest market share, thanks to stringent renewable‑integration mandates and a well‑established supply chain. North America’s growth will be underpinned by federal clean‑energy incentives and a resurgence of domestic manufacturing for semiconductor‑based power modules.

Key Recommendations for Stakeholders

Report Scope

This market research report offers a holistic overview of global and regional markets for the forecast period 2025–2032. It presents accurate and actionable insights based on a blend of primary and secondary research.

Key Coverage Areas:

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia‑Pacific: +91 9169164321

🔗 LinkedIn: Follow Us