Galvanized Gutter Repair Services Bixby, OK

Other |

2025-11-13 22:05:21

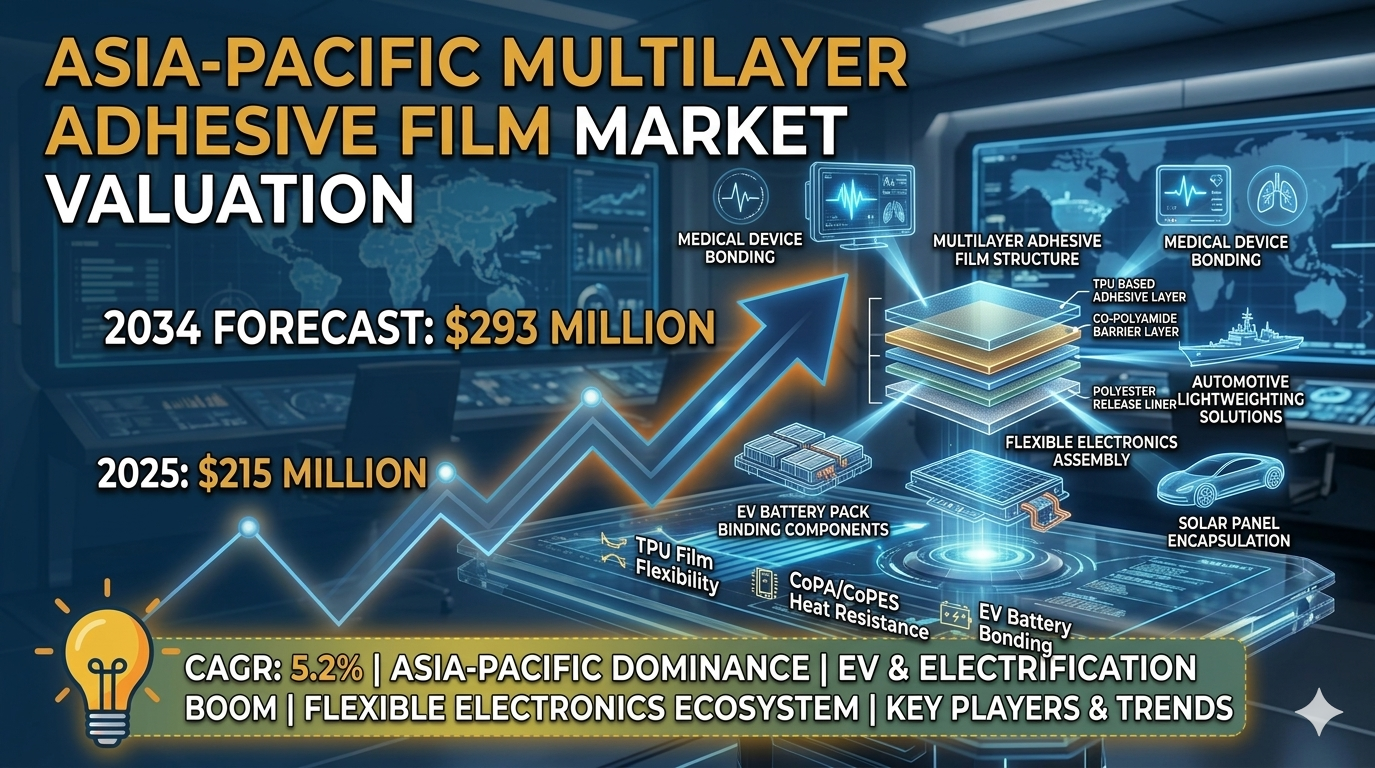

According to a new report from Intel Market Research, the Asia-Pacific multilayer adhesive film market was valued at USD 215 million in 2025 and is projected to reach USD 293 million by 2034, growing at a steady CAGR of 5.2% during the forecast period (2025–2034). This growth is propelled by the region’s dominant position in electronics manufacturing, rapid automotive sector expansion, and accelerating adoption of electric vehicles across China, Japan, South Korea, and India.

Multilayer adhesive films are engineered thermoplastic bonding materials that deliver controlled adhesion, structural integrity, and sealing performance in composite structures. They function as solid, pre‑metered adhesive layers that are activated by heat and pressure, offering a cleaner alternative to traditional liquid adhesives for textiles, plastics, metals, and paper substrates. Key material families include TPU‑based films, co‑polyamide (CoPA) and co‑polyester (CoPES) films, polyolefin/EVA films, and a range of specialty formulations developed for high‑performance applications.

📥 Download FREE Sample Report:

Asia-Pacific Multilayer Adhesive Film Market - View in Detailed Research Report

What is Multilayer Adhesive Film?

Multilayer adhesive film is a solid‑state bonding solution that integrates one or more adhesive layers between protective carrier films. When heat and pressure are applied, the adhesive layers melt and flow, forming a permanent bond without the mess or curing time associated with liquid adhesives. The multilayer construction enables designers to combine discrete functional layers-such as barrier, structural, and sealing films-within a single product, delivering a balance of mechanical strength, thermal stability, and environmental resistance.

This report provides an in‑depth view of the global and regional dynamics shaping the multilayer adhesive film market. It covers macro‑level market size and growth trends, as well as micro‑level details such as competitive landscape, technology road‑maps, key growth drivers, challenges, opportunities, and a thorough segmentation analysis.

Key Market Drivers

1. Expanding Flexible Electronics Ecosystem

The surge in demand for flexible smartphones, wearables, and roll‑to‑roll displays requires adhesive films that can endure repeated bending while maintaining strong bonding and thermal resistance. Manufacturers are turning to TPU‑based and co‑extruded films to meet these stringent performance criteria.

2. Automotive Lightweighting and Electrification

Automakers in the Asia‑Pacific region are intensifying efforts to reduce vehicle weight and improve fuel efficiency. Multilayer adhesive films enable the bonding of dissimilar materials-such as metal to composites-without fasteners, supporting the production of electric‑vehicle battery packs, interior trim, and exterior panels.

3. Renewable Energy and Solar Panel Manufacturing

The rapid growth of solar installations is driving demand for adhesive films that encapsulate photovoltaic cells, providing protection against moisture, UV exposure, and mechanical stress. Polyolefin/EVA films are commonly used in this application.

➤ Investments in consumer electronics, automotive manufacturing, and renewable energy are collectively accelerating the adoption of multilayer adhesive films across the Asia‑Pacific region.

Market Challenges

Raw Material Price Volatility

Fluctuations in petrochemical feedstock prices affect the cost of polymer substrates and adhesive components, compressing margins for manufacturers and creating uncertainty in pricing strategies.

Technical Integration Complexity

Integrating multilayer adhesive films into high‑density electronic assemblies demands precise process control and clean‑room environments. Smaller OEMs may lack the technical expertise or capital investment required to adopt these advanced solutions at scale.

Market Restraints

Environmental Regulations and Compliance

Stringent VOC limits, waste‑management policies, and recycling mandates in countries such as Japan, South Korea, and Australia increase compliance costs. Manufacturers must invest in low‑emission formulations and greener production processes, which can delay product launches.

Emerging Opportunities

Medical Devices and Advanced Packaging

The growing medical‑device sector in the region seeks adhesive films that are sterilizable, biocompatible, and capable of bonding flexible substrates for wearable health monitors. Simultaneously, the e‑commerce boom fuels demand for high‑performance packaging films that enhance product protection while supporting sustainability goals.

Collaborative research programs between universities and industry leaders are accelerating the development of bio‑based adhesives and recyclable multilayer structures, opening new avenues for product differentiation.

Segment Analysis

|

Segment Category |

Sub‑Segments |

Key Insights |

|

By Type |

|

TPU films are favored for flexibility and low VOC emissions; CoPA/CoPES provide high‑temperature resistance for automotive and renewable‑energy uses; polyolefin/EVA films dominate solar‑panel encapsulation. |

|

By Application |

|

Automotive and electronics drive the majority of demand, while medical and construction applications present high‑growth niches. |

|

By End User |

|

Tier‑1 automotive suppliers demand consistent thickness and automated handling; electronics OEMs prioritize low outgassing and thermal stability. |

|

By Functional Role |

|

Structural bonding films are critical for lightweight automotive components; barrier films enhance reliability of high‑frequency PCBs. |

|

By Technology |

|

Co‑extrusion enables precise multilayer construction for demanding electronic and medical applications; hybrid systems are emerging to improve sustainability. |

Competitive Landscape

Asia‑Pacific Multilayer Adhesive Film Market Competitive Overview

The market is led by a blend of global chemical giants and strong regional players. Toray Industries, ZACROS Co., Ltd. and Nitto Denko Corporation dominate the high‑performance segment, offering structural and specialty adhesive films tailored to electronics OEMs and Tier‑1 automotive suppliers. Chinese manufacturers such as Foshan Keben Industrial Co., Ltd. and Wenzhou Huate Adhesive Film Co., Ltd. provide cost‑effective solutions that support the rapid scaling of local electronics and packaging industries.

Other notable contributors include Namics Corporation, Covestro AG, Bostik (Arkema Group), Sika AG, and emerging innovators like Scapa Group plc. R&D centers in Singapore, South Korea, and Japan focus on low‑VOC formulations, bio‑based adhesives, and nano‑reinforced barrier layers, reinforcing the region’s technological edge.

List of Key Multilayer Adhesive Film Companies Profiled

Report Deliverables

📘 Get Full Report Here:

Asia-Pacific Multilayer Adhesive Film Market - View Detailed Research Report

Frequently Asked Questions

What is the current market size of the Asia‑Pacific multilayer adhesive film market? −

The market was valued at USD 215 million in 2025 and is projected to reach USD 293 million by 2034 with a CAGR of 5.2%.

Which companies are leading the market? +

Leading players include Toray Industries, ZACROS Co., Ltd., Nitto Denko Corporation, Covestro AG, and Bostik (Arkema Group).

What are the key growth drivers? +

Growth is driven by the region’s dominant electronics manufacturing base, rapid automotive sector expansion, and the accelerating adoption of electric vehicles.

Which region dominates the market? +

Asia‑Pacific is the fastest‑growing region, while Europe remains the largest by revenue.

What emerging trends are shaping the market? +

Emerging trends include development of TPU‑based, CoPA/CoPES and polyolefin/EVA films, specialty formulations for EV battery modules and high‑frequency PCB applications, and a strong focus on sustainability‑driven adhesive solutions.

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia‑Pacific: +91 9169164321

🔗 LinkedIn: Follow Us