Buy WGA Crystal Plus 20000 Box of 10 Online Easily

Other |

2026-03-17 10:29:01

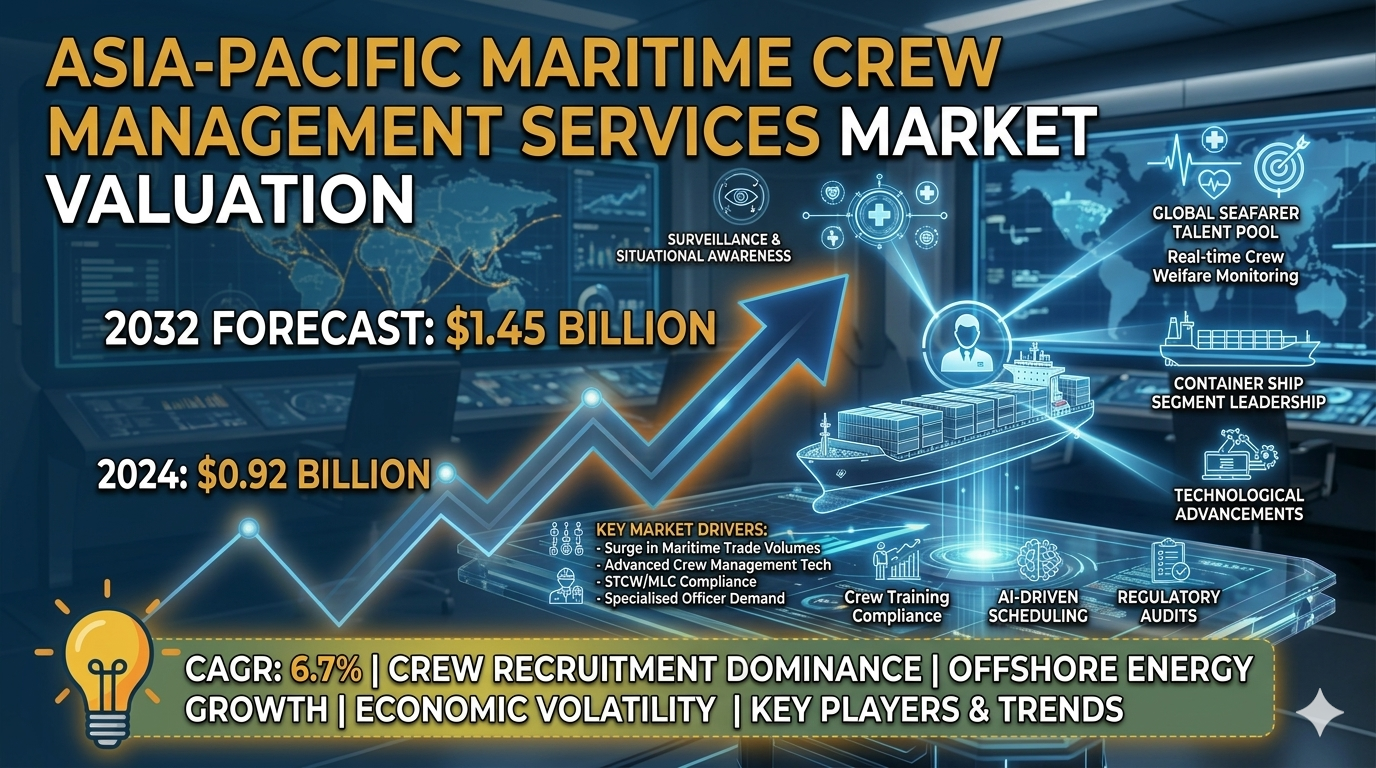

According to a new report from Intel Market Research, the Asia-Pacific Maritime Crew Management Services market was valued at USD 0.92 billion in 2024 and is projected to reach USD 1.45 billion by 2032, growing at a robust CAGR of 6.7% during the forecast period (2025–2032). This expansion is driven by accelerating seaborne trade, mounting demand for qualified seafarers, and the digital transformation of crew‑management operations across the region.

Maritime crew management services encompass a comprehensive suite of solutions for shipping companies, including crew recruitment, training, scheduling, payroll, and onboard welfare management. By ensuring compliance with international conventions such as STCW and MLC, these services help operators optimize vessel performance, reduce turnaround times, and mitigate regulatory risk. The sector is a cornerstone of regional trade, supporting the human capital needed for bulk carriers, container ships, and tankers that move goods between the world’s largest economies.

📥 Download FREE Sample Report:

Asia-Pacific Maritime Crew Management Services Market - View in Detailed Research Report

What is Maritime Crew Management Services?

Maritime Crew Management Services are specialized offerings that enable shipowners and operators to source, certify, train, and retain seafarers while maintaining full regulatory compliance. Service providers act as a single point of contact for crew lifecycle management, handling everything from recruitment in source countries such as the Philippines, India, and China to on‑board welfare, performance monitoring, and repatriation. By leveraging economies of scale and advanced digital platforms, these firms deliver cost‑effective, reliable staffing solutions that align with the increasingly complex demands of modern shipping.

The market’s steady upward trajectory reflects a confluence of macro‑economic and industry‑specific forces. Growing trade volumes in key Asian economies, stringent crew certification requirements under the STCW convention, and the rapid adoption of cloud‑based crew‑management software collectively underpin demand. Moreover, expanding fleets in China and South Korea, together with heightened safety and sustainability expectations, create a fertile environment for service providers to innovate and capture market share.

Key Market Drivers

Surge in Maritime Trade Activities

Over the past decade the Asia‑Pacific region has cemented its status as a global shipping hub. Record‑breaking cargo volumes, especially in containerized trade, have generated a pressing need for skilled crews capable of handling larger, more technologically advanced vessels. Shipping lines are turning to professional crew‑management firms to scale their workforce quickly while adhering to safety and compliance standards.

Adoption of Advanced Crew Management Technologies

Digital platforms that integrate AI‑driven scheduling, real‑time credential verification, and predictive analytics are reshaping the industry. Cloud‑based solutions reduce administrative overhead, improve crew utilisation, and enhance transparency for both owners and regulators. As operators seek to boost operational efficiency, technology‑enabled providers gain a competitive edge, accelerating market growth.

➤ Increased emphasis on safety, compliance, and workforce welfare in maritime operations necessitates professional crew‑management solutions in the Asia‑Pacific region.

Market Challenges

Complex Regulatory Environment

Navigating a mosaic of national and international maritime regulations poses a significant hurdle. Variations in certification standards, wage regulations, and labor laws across jurisdictions demand deep expertise and substantial investment from service providers to avoid costly compliance breaches.

Labor Shortages and Retention Issues

While the Asia‑Pacific benefits from a large seafarer pool, the industry faces periodic shortages of highly qualified officers, exacerbated by demanding work conditions and competition from other transport sectors. Retaining experienced crew remains a persistent challenge, influencing service providers’ ability to deliver uninterrupted fleet operations.

Market Restraints

Economic Volatility Impacting Maritime Operations

Fluctuating trade policies, geopolitical tensions, and pandemic‑related disruptions have occasionally curtailed cargo volumes, constraining shipping companies’ capital expenditure on crew‑management services. During downturns, operators may defer outsourcing initiatives, temporarily dampening market momentum.

Market Opportunities

Growth in Offshore Energy Sector

The expanding offshore oil, gas, and renewable energy projects in Australia, China, and Indonesia generate a distinct demand for specialised crews to support offshore support vessels, wind‑farm installation ships, and related platforms. These activities open avenues for crew‑management firms to diversify service portfolios and develop niche expertise.

Segment Analysis

Segment Analysis:

|

Segment Category |

Sub-Segments |

Key Insights |

|

By Type |

|

Crew Recruitment dominates in the Asia‑Pacific maritime market due to the region's vast seafarer supply, especially from the Philippines, India, and China.

|

|

By Application |

|

Container Ship Segment leads due to Asia‑Pacific’s prominent role in global container trade and expanding regional fleets.

|

|

By End User |

|

Shipowners form the leading client base, leveraging professional crew management to ensure regulatory compliance and efficient operations.

|

|

By Service Model |

|

Full Crew Management is preferred among Asia‑Pacific operators wanting end‑to‑end support to handle complex crewing challenges.

|

|

By Vessel Type |

|

Commercial Vessels constitute the largest segment due to the Asia‑Pacific’s dominant role in global maritime trade.

|

Regional Analysis

Southeast Asia remains the most dynamic hub for maritime crew management services within the Asia‑Pacific market. Singapore, Malaysia, and Indonesia benefit from bustling ports, extensive ship registries, and a growing demand for skilled seafarers. The strategic location along major shipping lanes encourages shipowners to partner with local agencies that provide end‑to‑end recruitment, training, and compliance solutions. Digital platforms have streamlined credential verification, while government‑industry collaborations are expanding the talent pipeline. Green‑shipping initiatives are also prompting agencies to embed sustainability modules into training curricula, aligning crew competencies with emerging environmental standards.

East Asia – encompassing China, Japan, and South Korea – features a mature fleet base and sophisticated regulatory frameworks. Shipowners prioritise crews with specialised technical expertise to operate LNG carriers and ultra‑large container ships. High‑skill talent, combined with strong safety cultures, sustains the region’s contribution to the market despite relatively higher labour costs.

South Asia – led by India and supported by Bangladesh and Sri Lanka – supplies a sizeable pool of cost‑effective seafarers. Recent shifts toward structured skill‑enhancement programmes, driven by collaborations between maritime universities and international crew firms, are raising the overall quality of the workforce.

Oceania – represented by Australia and New Zealand – distinguishes itself through rigorous safety regulations and a focus on offshore operations. Operators in this sub‑region favour locally sourced crew with extensive experience in challenging environments, creating a premium market segment.

Pacific Islands – including Fiji, Papua New Guinea, and Samoa – host a niche segment of regional shipping and offshore support vessels. Limited local training capacity has spurred partnerships with regional academies and foreign crew agencies to develop tailored upskilling programmes, ensuring a steady crew supply for remote operations.

Competitive Landscape

Leading Companies Shaping Asia‑Pacific Maritime Crew Management Services Market

Asia‑Pacific dominates the Maritime Crew Management Services market due to its substantial seafarer base, particularly from the Philippines, India, and China. Major regional players leverage strategic maritime hubs like Singapore and Hong Kong to coordinate global crew deployment and management, allowing a competitive and comprehensive service network. Leaders in this region offer extensive crew recruitment, certification management, training, scheduling, and onboard services, enabling compliance with international maritime standards and regulations. Companies such as ASP Crew Management and MISC Group have established strong footholds by providing localized and cost‑effective solutions tailored to the complex regulatory environments and diverse labour pools in Asia‑Pacific.

In addition to multinational firms, regional specialists emphasize niche competencies, including specialised training for LNG carriers and offshore vessels. Strategic investments in digital platforms to enhance operational efficiency and compliance tracking are a common focus among key players to address labour shortages and wage pressures. Firms such as Martracon and Marine Solutions capitalize on local training infrastructure and government collaboration to maintain a steady flow of certified seafarers. The competitive landscape is continuously evolving with alliances and technology adoption, positioning Asia‑Pacific companies as critical contributors to the global maritime crew management ecosystem.

List of Key Maritime Crew Management Companies Profiled

Frequently Asked Questions

What is the current market size of Asia‑Pacific Maritime Crew Management Services Market? −

The Asia‑Pacific Maritime Crew Management Services Market was valued at USD 0.92 billion in 2024 and is expected to reach USD 1.45 billion by 2032.

Which key companies operate in Asia‑Pacific Maritime Crew Management Services Market? +

Key players include V.Group, Wilhelmsen, ASP Crew Management, and MISC Group.

What are the key growth drivers? +

Key growth drivers include expansion of seaborne trade volumes, rising demand for skilled maritime labor, stricter STCW crew certification requirements, advancements in digital crew management platforms, and increasing fleet sizes in China and South Korea.

Which region dominates the market? +

Asia‑Pacific is the fastest‑growing region, while Europe remains a significant market.

What are the emerging trends? +

Emerging trends include digital crew management platforms, automation of scheduling, sustainability initiatives, and the integration of AI and IoT for real‑time crew performance monitoring.

📥 Get Full Report Here:

Asia-Pacific Maritime Crew Management Services Market - View Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia‑Pacific: +91 9169164321

🔗 LinkedIn: Follow Us