Best Cadet College Admission in 8th Class – Complete Guide for Students and Parents

Other |

2025-10-10 07:01:31

Surgical robotics represents a transformative leap in modern healthcare by merging highly sophisticated robotic systems with advanced surgical techniques to significantly enhance clinical outcomes. In essence, surgical robotics refers to computer-controlled mechanical devices designed to assist surgeons in performing complex and minimally invasive surgical procedures with improved precision, flexibility, and accuracy. These systems do not replace surgeons but empower them with enhanced visualization, better dexterity in constrained anatomical environments, and highly stable instrument control free from human tremors. Robotic-assisted platforms feature multiple components such as robotic arms, surgeon consoles, high-definition 3D vision systems, and integrated software that translates surgeon hand movements into micro-actions. This allows procedures that are traditionally difficult to perform manually to become safer and more efficient.

Surgical robotics have gained traction across numerous medical specialties including general surgery, urology, gynecology, orthopedics, neurology, cardiothoracic surgery, and even emerging fields such as ENT and ophthalmology. A widely recognized example is the da Vinci robotic platform, which revolutionized minimally invasive surgery by enabling smaller incisions, reduced trauma to surrounding tissues, minimized postoperative pain, shorter hospital stays, lower infection rates, and improved recovery outcomes. The integration of imaging technologies, AI-assisted guidance, augmented reality, and haptic feedback has further optimized surgical accuracy and elevated surgeon decision-making capabilities.

Get FREE Sample of this Report at https://www.intelmarketresearch.com/download-free-sample/13453/surgical-robotics-market

The market for surgical robotics continues to experience rapid growth due to the expanding demand for minimally invasive interventions globally. Patients increasingly prefer technology-enabled surgeries that ensure faster recovery and better cosmetic results. Moreover, hospitals are adopting robotic surgery systems as part of their competitive strategy to differentiate service offerings, boost procedure volumes, and improve operating room efficiency. Surgeons gain advanced tools that support complex anatomical navigation while reducing fatigue and enhancing ergonomics.

Demographic dynamics significantly reinforce demand, as aging populations are more susceptible to chronic illnesses requiring surgical correction — including cancer, degenerative orthopedic conditions, and cardiovascular disorders. Surgical robotics help reduce complication rates among elderly patients, ensuring better safety profiles. However, the field still faces crucial challenges such as high capital expenditure, lengthy training requirements, and the need for robust clinical evidence comparing long-term outcomes with traditional techniques. Despite these challenges, rapid technological innovation continues to expand capabilities, enabling the future vision of autonomous and telesurgery-driven robotics in which expert surgeons perform life-saving operations remotely in underserved regions.

Overall, the surgical robotics market is not just an evolution of tools but a redefining shift in surgical practice — one that aligns advanced engineering with precision medicine to unlock new possibilities in patient care.

Market Size

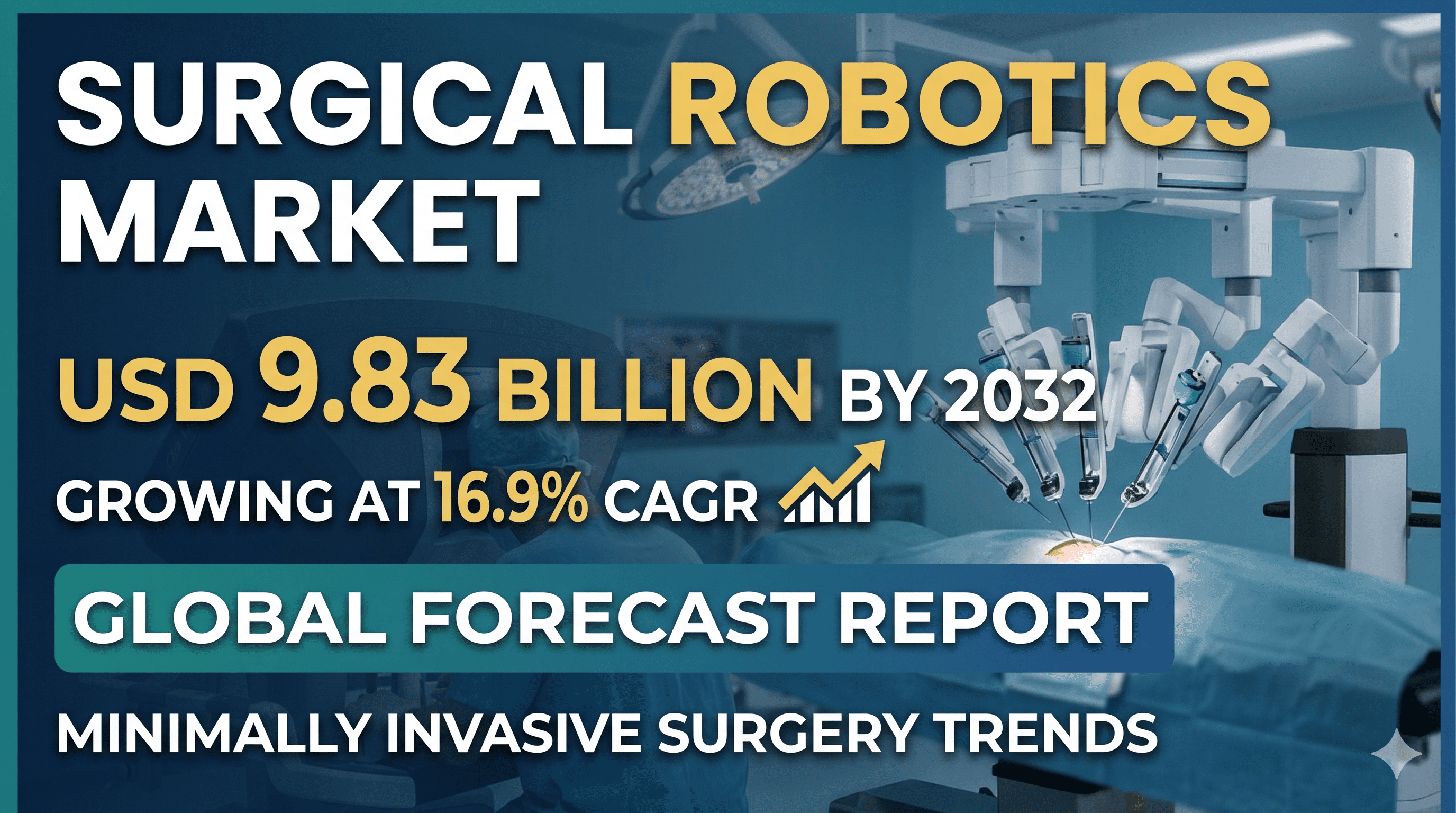

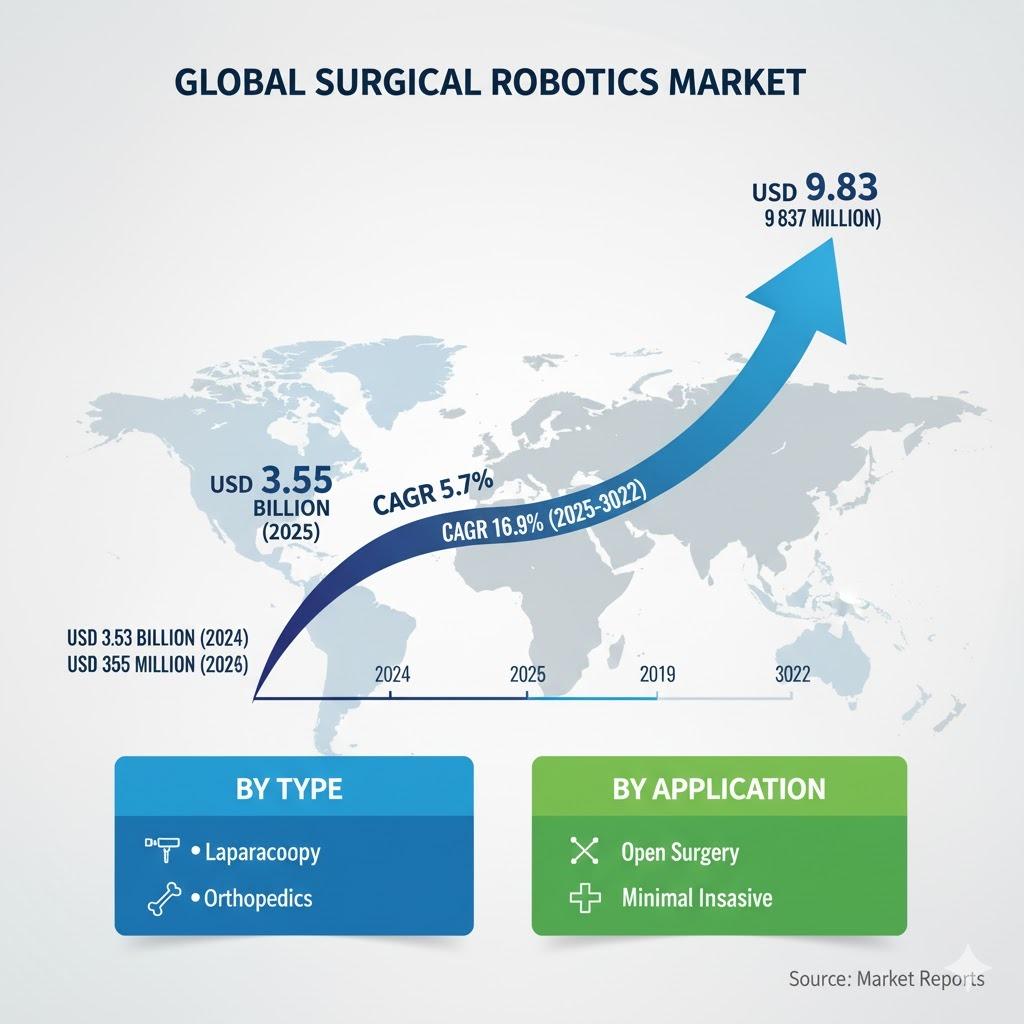

Global surgical robotics market has entered a high-growth phase driven by rapid clinical adoption and technological innovation. In 2024, the market was valued at USD 3.53 billion and is projected to rise to USD 3.95 billion in 2025, ultimately reaching USD 9.83 billion by 2032, exhibiting a robust CAGR of 16.9% over the forecast period. This acceleration is attributed to healthcare systems shifting toward minimally invasive surgeries that improve patient outcomes while reducing hospitalization costs.

Historical data reflects consistent growth as robotic platforms transitioned from specialized applications in urology and gynecology to wider usage in general surgery and orthopedics. Rising reimbursement support for select robotic procedures, particularly in developed markets, is enabling stronger procedural volume. Hospitals are increasingly integrating surgical robotics into oncology centers, cardiothoracic programs, and advanced orthopedic suites. The push toward value-based healthcare also aligns with robotic advantages such as fewer complications and higher precision, reducing postoperative care costs.

Capital investment into hospital infrastructure remains a crucial driver. Many healthcare providers calculate favorable long-term returns based on robotic system utilization rates. Additionally, recurring revenue from disposables and maintenance contracts forms a significant industry revenue pool, creating strong demand predictability for manufacturers.

Technological advancements such as scalable robotic architectures, modular systems, and AI-enhanced navigation provide compelling cost-benefit opportunities. Next-generation robots entering the market are designed to be more compact, affordable, and versatile, enabling wider adoption in ambulatory surgery centers — a fast-increasing market segment. Moreover, growing medical tourism in Asia and the Middle East further accelerates demand for technologically advanced surgical care.

Even though Europe and North America currently dominate market share, the fastest adoption trajectory is expected in Asia Pacific where healthcare expenditure is rapidly rising. The competitive landscape is also evolving, with emerging players introducing systems across specialized clinical fields that extend the market beyond traditional robotic solutions.

Overall, the expansion of robotic surgery platforms is driving the market toward becoming a mainstream component of global surgical workflows, with continued double-digit growth anticipated through 2032.

Regional Analysis

Regional market dynamics vary significantly based on healthcare infrastructure, regulatory systems, economic conditions, and physician training availability. North America currently leads the global surgical robotics market accounting for the largest revenue share due to strong healthcare investments, favorable reimbursement policies, and early technology adoption. The United States dominates within the region, with a vast installed base of robotic systems and continuous upgrades driven by high procedural volume in urology, gynecology, and colorectal surgery. Strong clinical evidence supporting robotic advantages further reinforces adoption.

Europe holds the second-largest share, supported by established healthcare systems, strong emphasis on surgical precision, and government initiatives for advanced medical infrastructure. Countries like Germany, France, the UK, and Italy are key adoption centers. However, slower reimbursement approvals compared to the U.S. occasionally restricts expansion.

The Asia Pacific region is expected to exhibit the fastest growth rate due to rising healthcare expenditures, increased incidence of chronic diseases, and expanding medical tourism. China, Japan, India, and South Korea are aggressively investing in robotics-enabled care. Domestic manufacturers in China and Japan are emerging and lowering cost barriers, making adoption more accessible for regional hospitals.

In Latin America, adoption is rising gradually, especially in Brazil and Mexico, as private healthcare groups seek differentiation. However, high costs remain a hurdle for public hospital penetration. Skilled surgeon shortages also limit operational utilization.

The Middle East and Africa remain at a developing stage but show strong strategic potential. Wealthy economies such as the UAE and Saudi Arabia are establishing advanced surgical centers, incorporating robotic systems into flagship hospital networks. Government-funded healthcare modernization programs are helping accelerate robotics adoption.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/medical-devices/13453/surgical-robotics-market

Urban-rural disparities remain a common challenge across all emerging markets. Training limitations also slow adoption since mastery of robotic procedures requires structured learning programs. Despite these challenges, increasing awareness among patients and surgeons continues to drive demand across all regions. Overall, strong investment momentum and ongoing technology advancements ensure that regional adoption patterns will keep evolving, with Asia Pacific becoming a major revenue contributor in the forecast period.

Competitor Analysis (in brief)

The surgical robotics market is dominated by pioneering companies that invest heavily in innovation, clinical validation, and global expansion strategies. Intuitive Surgical remains the clear leader with over 70% market share supported by its iconic da Vinci robotic platform, a massive installed base, and a mature ecosystem of disposable instruments and service offerings. Their continuous system upgrades and specialized procedure-focused tools create strong surgeon loyalty and high switching barriers.

Stryker holds a dominant position in orthopedic robotics with its Mako robotic-arm system designed for knee and hip surgeries. Its strong integration with implant systems enhances precision in joint replacement procedures. Medtronic, a major medical technology conglomerate, is expanding into soft-tissue robotics with the Hugo RAS platform aimed at competing directly against Intuitive on cost and flexibility. Johnson & Johnson has invested in digital surgery through its Ottava robotic platform currently under development, backed by the legacy of Ethicon’s surgical tools dominance.

Zimmer Biomet, Globus Medical, and Smith & Nephew focus strongly on orthopedic robotics, enhancing accuracy in spine and joint procedures. Asensus Surgical, formerly TransEnterix, is emphasizing digital-assisted surgery and augmented intelligence capabilities through its Senhance platform. CMR Surgical advances modular and cost-effective robotics with its Versius system, expanding in Europe, Asia, and the Middle East.

Competition is increasing as Asian manufacturers enter with more affordable robotic solutions targeting cost-sensitive markets. Software and AI-driven innovation is becoming a strategic differentiator as companies aim to build autonomous features and advanced intraoperative guidance systems. As technologies mature, the competitive environment is shifting from hardware-dominant models to integrated digital ecosystems that deliver superior clinical workflow efficiency and long-term economic value.

Global Surgical Robotics Market: Market Segmentation Analysis

This report provides a deep insight into the global Surgical Robotics Market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization.

The report structure also focuses on the competitive landscape of the Global Surgical Robotics Market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Surgical Robotics Market in any manner.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/medical-devices/13453/surgical-robotics-market

Market Segmentation (by Application)

Open Surgery

Minimal Invasive

Diagnostic Procedures

Market Segmentation (by Type)

Laparoscopy

Orthopedics

Neurology

Key Company

Intuitive Surgical Inc.

Stryker Corporation

Medtronic PLC

Zimmer Biomet Holdings Inc.

Johnson & Johnson

Siemens Healthineers AG

Smith & Nephew PLC

Asensus Surgical Inc.

THINK Surgical Inc.

CMR Surgical Limited

Accuray Incorporated

Medrobotics Corporation

TransEnterix Inc.

Globus Medical Inc.

Geographic Segmentation

North America

Europe

Asia Pacific

Rest of World

FAQ Section

What is the current market size of the Surgical Robotics Market?

As of 2024, the market size is USD 3.53 billion and expected to reach USD 9.83 billion by 2032.

Which are the key companies operating in the Surgical Robotics Market?

Leading players include Intuitive Surgical, Stryker, Medtronic, Zimmer Biomet, and Johnson & Johnson, among others.

What are the key growth drivers?

Growing preference for minimally invasive surgeries, aging population, technological advancements, and rising surgeon adoption.

Which region dominates the market?

North America currently leads due to strong infrastructure and reimbursement support, while Asia Pacific shows the fastest growth.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/medical-devices/13453/surgical-robotics-market

About Us

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in information technology, digital media solutions, and communication infrastructure. Our research capabilities include:

Real-time competitive benchmarking

Global technology adoption monitoring

Country-specific regulatory and market analysis

Over 500+ technology reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 International: +1 (332) 2424 294

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us