Complete Guide to Silicone Tube Diffuser Working, Features, and Applications

Home |

2026-05-08 04:57:34

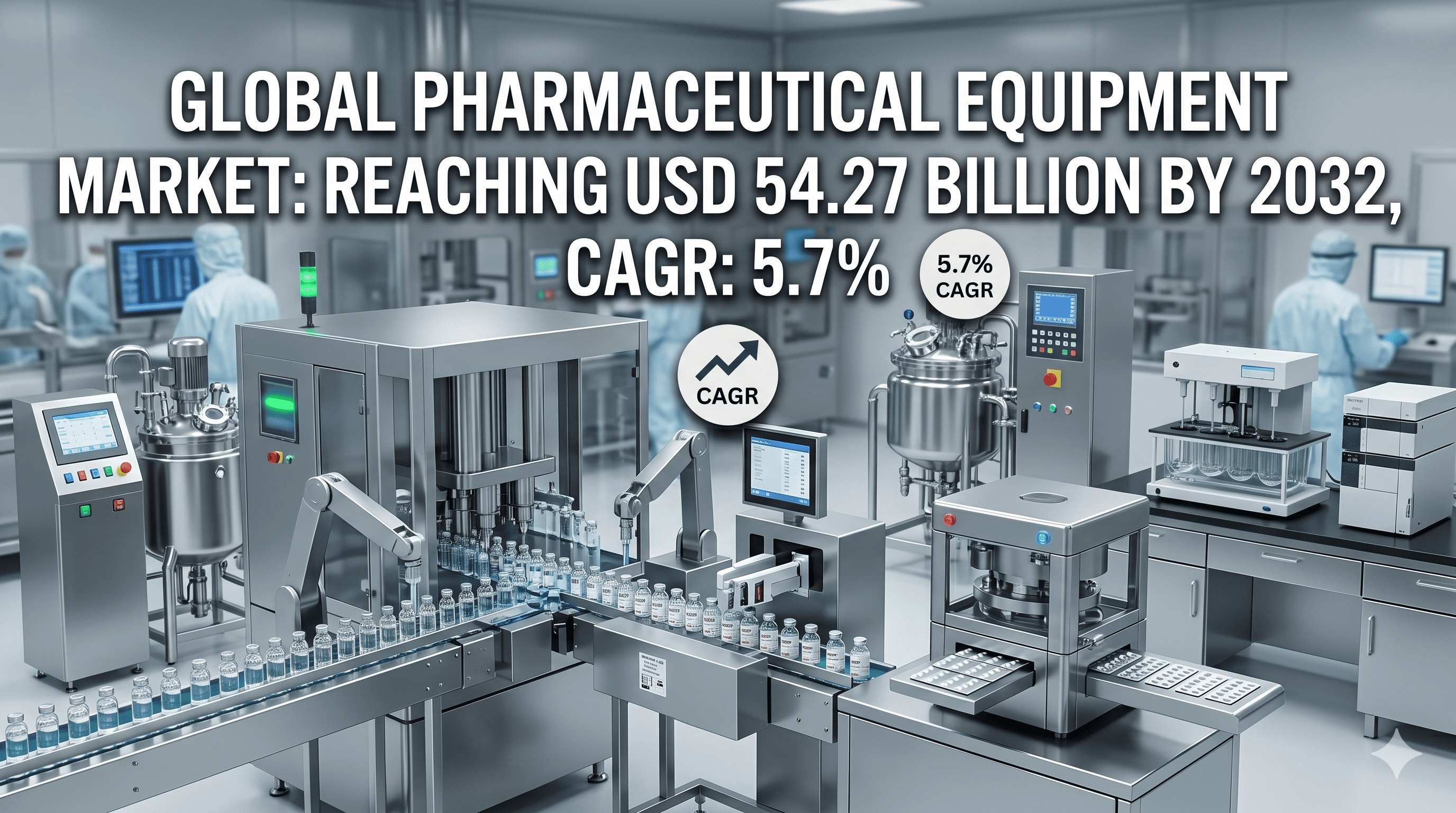

Global Pharmaceutical Equipment Market to Reach USD 54.27 Billion by 2032, Growing at a CAGR of 5.7%

The “pharmaceutical equipment market” refers to the global business ecosystem surrounding the design, manufacture, distribution and servicing of machinery, systems and instruments used in the production, testing, packaging, handling and quality-control of pharmaceutical products. These equipments span a broad set of functions and product categories—from bulk active pharmaceutical ingredient (API) processing, mixing and granulation, to filling, sterilization, inspection, packaging and labeling, as well as ancillary utilities such as water purification, clean-room HVAC, and laboratory instrumentation.

Get FREE Sample of this Report at https://www.intelmarketresearch.com/download-free-sample/13248/pharmaceutical-equipment-market

In more precise terms, the key product groups in this market typically include:

API Equipment: Systems for synthesis, separation, purification of active pharmaceutical ingredients.

Preparation Machinery: Equipment for formulation (e.g., mixing, granulation, compression, coating) of drugs.

Medicinal Crushing Machine: Machines to reduce particle size (e.g., mills, grinders) for tablet/capsule production.

Herbal Medicine Processing Machinery: Specialized equipment for processing herbal or botanical drugs (extraction, drying, standardisation).

Pharmaceutical Water Equipment: Systems for producing pharmaceutical-grade water (purified water, WFI – water for injection, distribution).

Pharmaceutical Packaging Machinery: Lines and machines for filling, sealing, labeling, blistering, cartoning and palletizing pharmaceutical products.

Drug Testing Equipment: Instruments and systems for quality control and release testing (e.g., HPLC, dissolution testers, spectrometers, microbial testers).

Others: Ancillary equipment, utilities, clean-room infrastructure, automation/robotics, maintenance tools.

In the broader sense, the pharmaceutical equipment market stands at the interface of pharmaceutical manufacturing, regulatory compliance, automation/Industry 4.0 adoption, and global health demand. Its growth is tied directly to pharmaceutical production volumes (including small molecules, generics, biologics), regulatory stringency (e.g., GMP/EMA/FDA), cost-pressure in production, and the shift toward more complex drug modalities (biologics, personalised medicine).

To summarise: the market is defined by all capital-equipment investments and supporting services directed at enabling the manufacturing, packaging and quality-assurance of pharmaceutical products globally.

Market Size

Market Size

As per available data, the global pharmaceutical equipment market was valued at USD 37.06 billion in 2024, and is projected to reach USD 54.27 billion by 2032, representing a compound annual growth rate (CAGR) of 5.7% over the forecast period.

To unpack this: the base year valuation is USD 37.06 billion (2024); the forecast for year 2032 is USD 54.27 billion; and the implied CAGR is 5.7 %. This offers an illustrative annualised growth trajectory: assuming year-0 = USD 37.06 billion, then year 8 = USD 54.27 billion.

Historical trend context: the market has been characterised by moderate growth, driven by increasing pharmaceutical production globally, rising regulatory demands, growing biologics manufacturing, and emerging-market ramp-ups. Fragmentation is high (no dominant single supplier) due to the wide variety of equipment types, tailored manufacturing needs, and regional variance in pharmaceutical infrastructure.

Key statistics worth highlighting:

2024 market size: USD 37.06 billion.

Forecast 2032 size: USD 54.27 billion.

CAGR: 5.7%.

Fragmentation: The top three companies in earlier years held only ~11 % of market share combined (e.g., in 2017: GE Healthcare ~4.18 %, Siemens ~3.30 %, Bosch ~3.10 %).

Regional dominance: For example, Europe held ~27.55 % of revenue in earlier data.

Key drivers: Growing pharmaceutical demand, biologics manufacturing, automation/Industry 4.0 adoption, emerging-market expansion.

Key constraints: Market fragmentation, high compliance/regulatory costs, lack of standardisation, steep capital investment.

One caveat: Some other reports cite different numbers (for example, one report projects a market value of ~USD 52 billion in 2024 and USD 68.2 billion by 2035, with a much lower CAGR of ~2.5% – showing wide variation across research providers). But for the purposes of this article we rely on the stated USD 37.06 billion → USD 54.27 billion at CAGR 5.7 % as the base scenario.

Regional Analysis

Regional Analysis

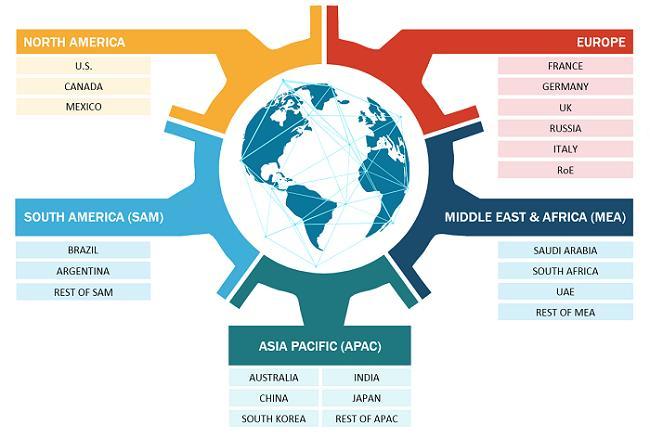

The global pharmaceutical equipment market is inherently international, with differential growth rates, equipment demand profiles, regulatory environments and manufacturing capacities across major geographies. Below is an analysis of key regions: North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

North America, led by the United States and Canada, remains one of the most mature markets for pharmaceutical equipment. Key features:

High regulatory stringency (e.g., Food and Drug Administration (FDA) in the U.S.), which drives frequent upgrades, replacement of older equipment, and demand for advanced, compliance-capable systems (sterility assurance, clean-rooms, automation).

High concentration of large pharmaceutical and biotechnology companies, biologics production, contract manufacturing organisations (CMOs/CDMOs) with sophisticated manufacturing lines.

Demand is for high-precision, high-performing equipment (e.g., aseptic fill-finish lines, high-end inspection systems, real-time analytics).

Growth is moderate (given maturity) but stable, and often involves replacement/retrofit rather than entirely new builds.

Supply chain and equipment manufacturing infrastructure is well-established.

Europe has historically held a significant revenue share (for example one earlier figure – ~27.55 % of global revenue). Key features:

Strong pharmaceutical manufacturing base (Germany, France, UK, Italy) and stringent regulatory oversight (European Medicines Agency (EMA)).

Demand for advanced equipment, particularly in biologics/sterile injectables segments, and packaging/serialization driven by EU regulations.

Emerging manufacturing investment in Eastern Europe and pharmaceuticals outsourcing to Central/Eastern Europe.

Growth is moderate; however emerging sub-segments (e.g., continuous manufacturing, modular plants) present expansion pathways.

The Asia Pacific region is one of the fastest-growing regions in the pharmaceutical equipment market. Key characteristics:

Countries such as China, India, Japan, South Korea, Southeast Asia are ramping up pharmaceutical manufacturing capacity—both generics and biologics.

Cost-efficient manufacturing base, increasing regulatory harmonization, growing exports of pharmaceuticals drive equipment demand.

Investments in emerging countries, green-field facilities, contract manufacturing, and regional supply chain shifts (e.g., to India and Southeast Asia) accelerate equipment purchases.

Growth rates tend to exceed those in North America/Europe, driven by base-case low equipment penetration, increasing manufacturing infrastructure development, modernization of older plants, and government initiatives (e.g., “Make in India”).

For example, some sources report high growth in Asia-Pacific for packaging equipment and processing equipment segments.

While smaller by market size compared to North America/Europe/Asia Pacific, Latin America has growth potential:

Countries such as Brazil, Argentina are seeing increased healthcare spending, local pharmaceutical manufacturing expansions, and imports of advanced equipment.

Challenges include weaker regulatory environments, slower adoption of advanced technologies, and economic/political volatility.

Equipment demand often leans toward retrofit, cost-effective solutions rather than ultra-high end.

Growth is moderate but offers opportunity for specialised equipment vendors who can adapt cost models.

This region also offers emerging opportunities, though at slower pace and from lower base:

Countries such as Saudi Arabia, UAE, Turkey, Israel in the Middle East are developing pharmaceutical manufacturing infrastructure—often supported by government initiatives.

In Africa, drug-manufacturing capacity is still limited but improving; equipment demand may focus on generics manufacturing and packaging/labeling.

Key constraints: regulatory complexity, lower capital availability, lower volumes, supply-chain/logistics challenges.

Nonetheless, growth is expected as global pharmaceutical supply chains diversify and localisation efforts expand.

In essence: North America and Europe remain large, mature markets with steady but slower growth; Asia Pacific represents the fastest-growing region with strong upside; Latin America and Middle East & Africa are smaller but offer incremental growth opportunities.

Strategic insight: For equipment manufacturers, the optimal regional strategy may involve combining stable revenue streams from North America/Europe with aggressive growth initiatives focused on Asia Pacific, and selective entries into Latin America and Middle East & Africa for diversification and long-term potential.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/machines/13248/pharmaceutical-equipment-market

Competitor Analysis (in brief)

Competitor Analysis (in brief)

The pharmaceutical equipment market is highly fragmented, spanning many niche product categories and custom-tailored manufacturing solutions. No single company dominates across all equipment types and regions. Here’s a concise overview of major players, their strategies and competitive positioning:

GE Healthcare – Historically one of the leading equipment providers, especially in pharmaceutical manufacturing systems and process control. Earlier data cited ~4.18 % market share (2017) in the broader equipment market.

Siemens – Strong in automation, process control, instrumentation, providing solutions for pharmaceutical plants seeking Industry 4.0 upgrades. ~3.30 % market share in 2017 in the cited dataset.

Bosch – Known for packaging machinery, inspection systems, manufacturing infrastructure. ~3.10 % market share in 2017 according to earlier dataset.

Sartorius AG – Strong in bioprocessing equipment (especially for biologics) and high-end pharmaceutical manufacturing.

Shimadzu Corporation – Japanese player with strong presence in analytical instruments, drug-testing equipment, and QC instrumentation.

Shinwa Corporation – Regional Japanese equipment manufacturer focusing on specific pharmaceutical production machinery.

ACG Worldwide – Global supplier of machinery & packaging solutions for pharmaceuticals, especially for tablets, capsules, blister lines.

Tofflon – Chinese company expanding in sterile production equipment, and equipment for injectables.

Bausch+Ströbel Maschinenfabrik GmbH – German specialist in packaging and filling systems for pharmaceuticals.

GEA Group AG – German engineering group with strong capabilities in process engineering for pharmaceuticals, especially upstream processing.

Truking – Chinese manufacturer of pharmaceutical packaging and tablet/capsule production lines.

Chinasun – Chinese company manufacturing tablet presses, granulators, downstream equipment for pharma.

Bohle Group – German group specialising in equipment for downstream processing (e.g., tablet presses, coating machines) for pharmaceuticals.

Sejong Pharmatech Co., Ltd. – South Korean company focused on tablet/capsule equipment, mixing systems.

SK Group – South Korean conglomerate with growing divisions in pharmaceutical-manufacturing equipment.

Differentiation via technology/automation: Many leading firms compete on offering high-end automation, robotics, data analytics, integration with smart manufacturing, and regulatory compliance (GMP, serialization).

Geographic expansion/ localisation: Chinese and Indian manufacturers (e.g., Tofflon, Truking, Chinasun) are leveraging lower-cost manufacturing, local market insight, and growing regional demand to challenge established players.

Service/After-market support: Given the high-capital nature of equipment, offering maintenance, retrofits, spare-parts, upgrades and remote analytics is a key competitive strategy.

Modular, flexible manufacturing lines: With increasing demand for smaller batches, biologics, and contract manufacturing, vendors offering modular, quickly reconfigurable equipment suites gain an edge.

Strategic partnerships/M&A: Some vendors pursue acquisitions or alliances to broaden their offering (for example in packaging + automation + software).

Focus on niche segments: Given fragmentation, many vendors specialise (e.g., packaging machines, inspection systems, water-for-injection systems) rather than trying to cover full plant lines.

Get the Complete Report & TOC at https://www.intelmarketresearch.com/machines/13248/pharmaceutical-equipment-market

As cited, in an earlier dataset (2017) the top three players (GE Healthcare ~4.18 %, Siemens ~3.30 %, Bosch ~3.10 %) together held less than 11% of the market—highlighting the fragmentation. Over time, this fragmentation continues because of the wide range of equipment categories, customisation and regional variations.

In sum: for a company entering this market (or for investors analyzing it), the landscape is competitive, multidisciplinary (mechanical, automation, software, process engineering), regionally diverse, and technologically evolving.

Global Pharmaceutical Equipment: Market Segmentation Analysis

This report provides a deep insight into the global pharmaceutical equipment market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global pharmaceutical equipment market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the pharmaceutical equipment market in any manner.

Market Segmentation (by Application)

Retain this section exactly as provided, without changes or additional explanations.

Market Segmentation (by Type)

Keep this section unaltered with no additional explanations or modifications.

Key Company

Maintain this section intact, with no changes or additions.

GE Healthcare

Siemens

Bosch

Sartorius

Shimadzu

Shinwa

ACG

Tofflon

Bausch+Stroebel

GEA

Truking

Chinasun

Bohle

Sejong Pharmatech

SK Group

Geographic Segmentation

Preserve this section as-is, without edits or omissions.

North America: U.S., Canada, Mexico

Europe: Germany, France, U.K., Italy, Russia, Nordic Countries, Benelux, Rest of Europe

Asia: China, Japan, South Korea, Southeast Asia, India, Rest of Asia

South America: Brazil, Argentina, Rest of South America

Middle East & Africa: Turkey, Israel, Saudi Arabia, UAE, Rest of Middle East & Africa

Additional Insights — Drivers, Challenges & Opportunities

While the above structured sections cover definition, size, regional breakdown and competitor landscape, it’s important to deepen discussion on what is driving the market, what restraints exist, and where opportunities lie.

Global Pharmaceutical Industry Expansion: The pharmaceutical industry is ever-growing: ageing populations, rising prevalence of chronic and lifestyle diseases, expanding healthcare access in emerging economies all contribute to greater demand for medicinal products. As drug production volumes increase, the need for manufacturing equipment correspondingly grows.

Technological Advancements in Equipment: Advances in automation, robotics, digital manufacturing, data analytics, real-time monitoring systems, and smart factory integration are transforming pharmaceutical equipment. Equipment that offers higher precision, lower downtime, better compliance, faster change-overs (especially for biologics and small batches) is highly sought after.

Shift to Biologics, Complex Drugs and High-Value Products: Biologics, cell & gene therapies, personalised medicine require more sophisticated manufacturing and testing equipment (e.g., single-use systems, modular lines, multi-product capability). This raises the value of equipment per production line, increasing overall equipment market size.

Emerging Markets & Infrastructure Build-out: Emerging economies (Asia Pacific, Latin America, Middle East & Africa) are investing in healthcare infrastructure and pharmaceutical manufacturing capacity. As more facilities get built, there is latent demand for equipment and the associated service/maintenance ecosystem.

Regulatory Compliance & Quality Assurance: Pharmaceutical manufacturers face increasing regulatory scrutiny (GMP, serialization, data integrity) which pushes them to upgrade or replace older equipment, invest in inspection/quality control instrumentation, and adopt new manufacturing paradigms (continuous manufacturing).

COVID-19 Pandemic Impact: The COVID-19 pandemic accelerated investment in vaccine production, sterile injectable manufacturing, contract manufacturing and equipment upgrades/modular lines, thereby giving a boost to equipment demand in the short to medium term.

High Competition and Market Fragmentation: As noted, the market is highly fragmented and competitive. Many specialised equipment categories exist, which means margins can be pressured. Smaller players may struggle to differentiate.

Regulatory Compliance Costs: Equipment manufacturers and end-users must meet stringent regulatory and quality standards. For manufacturers this increases R&D, certification, validation costs; for end-users it increases total cost of ownership.

Fragmentation and Standardisation Issues: Given the wide variety of equipment types and custom manufacturing needs, there is a lack of universal standards or interoperability across systems — which can increase integration costs, slow adoption, and reduce economies of scale.

Capital Intensity & Longer Payback: Pharmaceutical manufacturing equipment is highly capital intensive and often has long payback periods. For smaller producers or in lower-income regions, this may slow investment.

Legacy Equipment Replacement Cycles: In some mature markets, much equipment has already been installed; new growth may be more replacement/upgrade rather than new build – which can dampen growth rates.

Economic/Political/Trade Risks: Equipment manufacturers operating globally must navigate trade tariffs, supply-chain disruptions, component shortages, currency fluctuations, and shifting regulatory regimes — especially with increasing focus on localisation of pharmaceutical manufacturing.

Emerging Market Expansion: Fast-growing pharmaceutical manufacturing in Asia (China, India, Southeast Asia) and parts of Latin America/Middle East provide large untapped equipment markets. Manufacturers who tailor cost-effective, flexible solutions for these markets can capture growth.

Automation, Digitalisation & Smart Factories: Equipment suppliers that embed IoT, AI, remote monitoring, predictive maintenance, and real-time quality control into their offerings will be well-positioned to win business from manufacturers seeking operational efficiency.

Continuous Manufacturing & Modular Plants: The shift from batch to continuous processing, and the rise of modular manufacturing plants (especially for biologics/injectables), open new demand for specialised equipment and retrofits.

Service & Lifecycle Management: With installed base growth, demand for maintenance, upgrades, spare-parts, lifecycle management, retrofit packages and digital servicing is increasing — offering recurrent revenue streams for equipment vendors.

Sustainability and Green Manufacturing: Equipment that enables energy efficiency, reduced water usage (especially for pharma water systems), lower waste, modular clean-rooms, and recycling – these features are becoming differentiators and may command premium pricing.

Contract Manufacturing Organisations (CMOs/CDMOs): The increasing outsourcing of pharmaceutical manufacturing to CMOs/CDMOs is driving demand for flexible, multi-product equipment lines — this presents opportunities for equipment vendors to provide modular, quick-change systems.

Strengths: Growing pharmaceutical industry demand; advanced technology adoption; global footprint.

Weaknesses: High fragmentation; long lead-times; high capital cost; integration complexity.

Opportunities: Emerging markets; digitalisation; continuous manufacturing; service revenue.

Threats: Regulatory changes; economic/trade risks; alternative business models (contract manufacturing) reducing equipment spend by end-users; competitive pressure from low-cost regional suppliers.

Conclusion

The global pharmaceutical equipment market presents a compelling growth trajectory—valued at roughly USD 37.06 billion in 2024 and expected to reach USD 54.27 billion by 2032 at a 5.7% CAGR. Growth is underpinned by the expansion of the pharmaceutical and biopharmaceutical industry, global manufacturing infrastructure development, regulatory pressure for modernisation, and the adoption of advanced, automated manufacturing technologies.

From a strategic perspective, equipment manufacturers and investors should focus on: capturing growth in emerging regions (Asia Pacific, Latin America, Middle East/Africa), embedding digital and automation capabilities into equipment portfolios, cultivating service/after-market business models, and aligning with the shift toward biologics, continuous manufacturing and modular plants. At the same time, mindful navigation of regulatory complexity, high capital cost barriers, integration challenges and competitive fragmentation will be essential to sustainable success.

For end-users (pharmaceutical manufacturers), this also means equipment selection must increasingly prioritise flexibility, automation, regulatory compliance, cost efficiency and scalability — rather than simply capacity expansion. The equipment market is evolving from high-volume commodity machines to smarter, connected, modular, multi-product systems.

If you are considering entry into this market — as a manufacturer, investor, consultant or strategist — this is a “must-read” space, especially in light of the competitive landscape, technological disruption and emerging region opportunity.

FAQ

What is the current market size of the pharmaceutical equipment market?

The market was valued at approximately USD 37.06 billion in 2024 (based on available data) and is forecast to grow to USD 54.27 billion by 2032 at a CAGR of 5.7%.

Which are the key companies operating in the pharmaceutical equipment market?

Key companies include (but are not limited to):

GE Healthcare

Siemens

Bosch

Sartorius AG

Shimadzu Corporation

Shinwa Corporation

ACG Worldwide

Tofflon

Bausch+Ströbel

GEA Group AG

Truking

Chinasun

Bohle

Sejong Pharmatech

SK Group

What are the key growth drivers in the pharmaceutical equipment market?

The main drivers are: expanding global pharmaceutical/biopharmaceutical production; regulatory compliance requiring equipment upgrades; technology advancement (automation, robotics, smart manufacturing); emerging-market manufacturing infrastructure build-out; and increased demand for biologics, continuous manufacturing and flexible production lines.

Which regions dominate the pharmaceutical equipment market?

North America and Europe currently hold significant market shares due to mature pharmaceutical manufacturing and regulatory environments. The Asia Pacific region, however, is among the fastest-growing regions, driven by increasing manufacturing capacity, cost advantages, and emerging market expansion. Latin America and Middle East & Africa also present growth opportunities from a lower base.

What are the emerging trends in the pharmaceutical equipment market?

Emerging trends include:

The shift from batch manufacturing to continuous processing and modular manufacturing plants.

Increased use of automation, robotics, real-time analytics and IoT connectivity in equipment.

Growth in single-use systems (especially in biologics manufacturing).

Higher demand for flexible, multi-product production lines (especially in CMOs/CDMOs).

A growing service/lifecycle-management business model for equipment vendors.

Greater focus on sustainable manufacturing: energy/water reduction, equipment lifecycle optimisation.

Regionalisation and diversification of manufacturing (so equipment demand shifts geography, e.g., to Asia Pacific, Latin America, Middle East).

Get the Complete Report & TOC at https://www.intelmarketresearch.com/machines/13248/pharmaceutical-equipment-market

About Us

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in information technology, digital media solutions, and communication infrastructure. Our research capabilities include:

Real-time competitive benchmarking

Global technology adoption monitoring

Country-specific regulatory and market analysis

Over 500+ technology reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 International: +1 (332) 2424 294

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us