A Full Overview on Schwab Online Trading and Schwab Trading Account

Networking |

2026-04-03 06:07:07

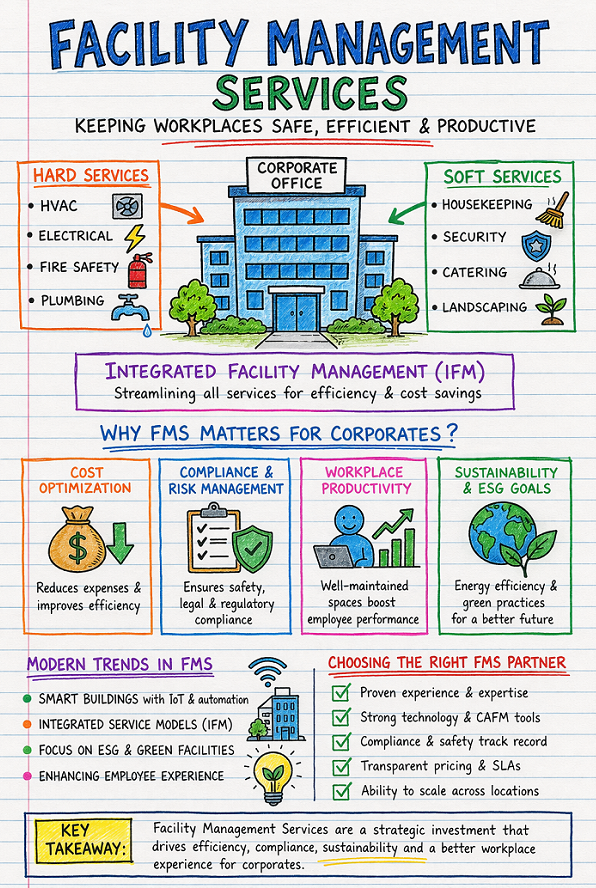

The global facility management services market is a sprawling and highly competitive arena, with the overall Facility Management Services Market Share fragmented among a diverse ecosystem of providers. The landscape is not dominated by a single entity but is instead comprised of several tiers of competitors, each with a distinct strategy and target audience. At the top of the pyramid are a handful of massive, global, publicly-traded companies that command a significant portion of the market, especially within the Fortune 500 segment. Below them are strong regional champions that have a deep presence in a specific continent or group of countries. Finally, the base of the pyramid is made up of a vast number of local, specialized service providers who often cater to small and medium-sized enterprises (SMEs) or offer a niche service. This multi-layered structure creates a dynamic competitive environment where scale, specialization, technological prowess, and customer relationships all play a crucial role in the battle for market share.

The largest portion of the market share, particularly in the Integrated Facility Management (IFM) space, is controlled by a group of global real estate and service giants. This elite group includes companies like CBRE Group, JLL, Cushman & Wakefield, Sodexo, Compass Group, and ISS A/S. These titans leverage their immense scale, global footprint, and extensive service portfolios to serve large multinational corporations that require consistent, high-quality service across their entire global real estate portfolio. Their core strategy revolves around providing a fully integrated, end-to-end solution that combines traditional FM services with higher-value corporate real estate (CRE) services, such as transaction management, strategic consulting, and project management. By positioning themselves as strategic partners rather than just service vendors, they embed themselves deeply within their clients' operations. Their ability to invest heavily in technology platforms, data analytics, and global best practices allows them to deliver sophisticated, data-driven solutions that smaller competitors struggle to replicate, solidifying their dominance in the large enterprise market.

Despite the dominance of the global giants, strong regional and local service providers play a vital role in the market and hold a significant collective share. These companies thrive by focusing on specific geographic areas where they possess deep market knowledge, strong local relationships, and a nuanced understanding of the regional regulatory landscape. Unlike the global players who may offer a standardized global model, regional providers often offer greater flexibility and customization to meet the specific needs of their clients. They are particularly successful in serving the SME market, which may not require a global service footprint and often prefers a more personal, high-touch service model. Furthermore, many smaller companies specialize in a particular niche service, such as cleanroom maintenance for the pharmaceutical industry or critical systems management for data centers. By building a reputation for excellence in a specific domain, these specialists can effectively compete and win business, even against much larger, generalist competitors, ensuring the market remains vibrant and diverse.

In this fiercely competitive environment, providers are employing several key strategies to capture and grow their market share. Mergers and acquisitions (M&A) are a primary tool for consolidation, allowing large players to quickly expand their geographic reach, broaden their service capabilities, or acquire innovative technologies. The acquisition of smaller, specialized firms is a common tactic to enter new markets or service lines. Technology adoption, particularly in the "proptech" (property technology) space, has become a critical differentiator. Providers who can effectively leverage IoT, AI, and advanced analytics to deliver predictive maintenance, energy savings, and superior workplace experiences have a significant competitive advantage. Finally, there is a notable shift in commercial models, moving away from traditional, input-based contracts (paying for labor hours) towards outcome-based or performance-based contracts. In this model, the provider's compensation is tied to achieving specific, measurable key performance indicators (KPIs), such as energy savings, asset uptime, or employee satisfaction, aligning the provider's incentives directly with the client's business goals and creating a stronger, more strategic partnership.

Explore Our Latest Trending Reports!