Panduan Lengkap Memulai di mejahoki slot untuk Pemula

Other |

2026-04-08 04:35:45

The Rapid Evolution of Buy Now Pay Later (BNPL)

Buy Now Pay Later (BNPL) has transitioned from a niche fintech offering into a mainstream payment mechanism reshaping global consumer finance. What began as a simple “pay-in-four” installment model has evolved into a broader ecosystem of flexible credit solutions embedded directly into digital commerce. Today, BNPL is not just about convenience—it is a structural shift in how consumers access and manage short-term credit.

The acceleration of e-commerce, combined with the demand for frictionless checkout experiences, has been a primary catalyst. BNPL integrates seamlessly into online platforms, allowing consumers to split payments without traditional credit card barriers. This ease of use, coupled with minimal onboarding requirements, has significantly expanded its user base across demographics, especially among younger consumers and those underserved by conventional banking systems.

Growth Momentum and Market Expansion

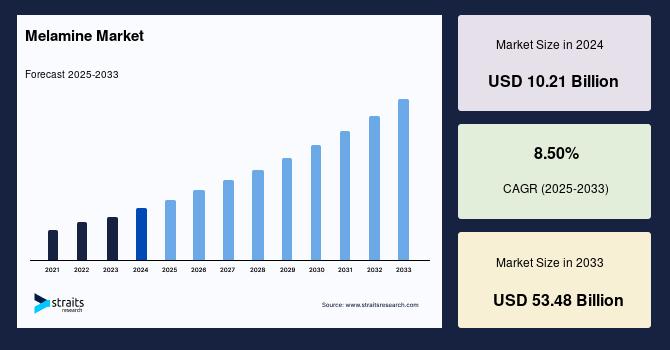

The scale of BNPL’s growth highlights its transformative impact. The global buy now pay later market size is projected to reach USD 80.15 billion by 2033, growing at a CAGR of 27.0% from 2025 to 2033, according to Grand View Research.

This rapid expansion is driven by increasing consumer preference for flexible payment options and the rising cost of living, which has made deferred payment solutions more attractive. Retail remains the dominant sector, but adoption is expanding into healthcare, travel, and even essential spending categories.

Additionally, BNPL is no longer confined to online channels. Point-of-sale (POS) integration in physical retail environments is gaining traction, enabling real-time financing decisions in-store. This omnichannel presence is critical, as it aligns with hybrid shopping behaviors where consumers move fluidly between digital and physical retail experiences.

Key Trends Reshaping the BNPL Landscape

One of the most notable trends is the diversification of BNPL providers into full-service fintech platforms. Companies are increasingly offering debit-like products, longer-term financing, and personalized financial tools. This shift reflects a strategic move to deepen customer engagement and generate sustainable revenue streams beyond transaction fees.

Another emerging trend is the expansion of BNPL into everyday spending. What was once used primarily for discretionary purchases like fashion and electronics is now being applied to groceries, food delivery, and utilities. This signals both increased adoption and changing consumer financial behavior under economic pressure.

At the same time, partnerships between fintech firms, retailers, and digital platforms are accelerating ecosystem growth. BNPL is becoming embedded not just in checkout systems but across entire customer journeys, including travel booking, subscription services, and mobile apps. This embedded finance model is expected to define the next phase of industry evolution.

Regulatory scrutiny is also intensifying globally. Authorities are focusing on transparency, responsible lending, and credit reporting practices. Rather than slowing growth, this has prompted innovation in risk assessment, user education, and compliance frameworks, ultimately strengthening consumer trust.

Consumer Behavior and Financial Implications

BNPL’s appeal lies in its ability to reduce the psychological friction of spending. By breaking payments into smaller, interest-free installments, it increases purchasing power and encourages higher transaction values. Merchants benefit from improved conversion rates and customer retention, making BNPL a powerful commercial tool.

In essence, the market can be understood as follows: BNPL allows consumers to access immediate purchasing power while distributing financial impact over time, creating a mutually beneficial dynamic for both buyers and sellers. This flexibility has made it particularly attractive in inflationary environments where consumers seek to manage cash flow more carefully.

However, this convenience comes with risks. Rising usage for essential expenses and increasing instances of missed payments highlight concerns around overextension and financial discipline. Critics argue that while BNPL enhances accessibility, it may also obscure the true cost of consumption and contribute to short-term debt accumulation.

The Road Ahead: Integration and Maturity

Looking forward, BNPL is expected to become deeply integrated into the broader financial services ecosystem. The convergence of BNPL with digital wallets, traditional banking, and credit infrastructure will redefine how consumers interact with money. In regions like Asia-Pacific, rapid digital adoption and a large underbanked population present significant growth opportunities.

At the same time, the industry is moving toward maturity. Providers are refining credit models, improving underwriting standards, and exploring profitability beyond promotional incentives. The shift toward regulated, transparent, and sustainable models will likely determine long-term success.

Ultimately, BNPL is no longer just a payment option—it is a reflection of evolving consumer expectations in a digital-first economy. As financial technology continues to innovate, BNPL will remain at the forefront, balancing convenience, accessibility, and responsibility in the future of global commerce.