WhatsApp Recommends VPNs: Bypass Blocks

Games |

2026-03-06 09:54:38

Credit underwriting — the process of evaluating whether to extend credit to a borrower or customer, and on what terms — is one of the highest-stakes analytical functions in any business. A well-underwritten credit portfolio generates predictable revenue and manageable risk. A poorly underwritten one accumulates delinquencies, erodes margins, and ultimately produces the write-offs and cash flow disruption that characterise chronically underperforming AR functions.

At the heart of effective credit underwriting is the ability to assess a credit applicant's financial health quickly, accurately, and consistently. Financial Ratios, applied within a structured framework, are the most reliable tool available for this purpose. They translate the complexity of financial statements into a set of comparable, interpretable metrics that support evidence-based credit decisions rather than subjective judgments based on incomplete information.

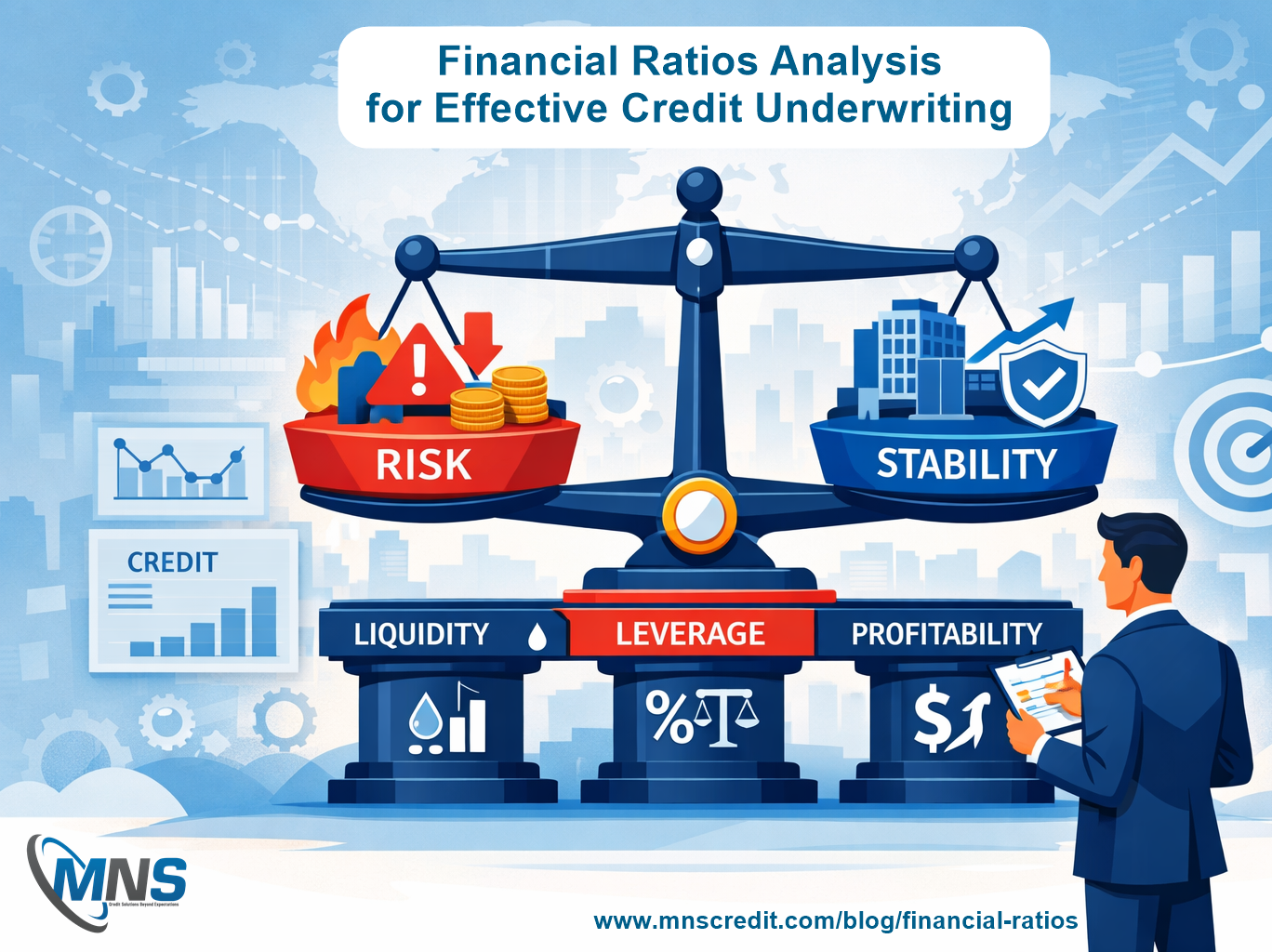

A comprehensive credit underwriting framework assesses Financial Ratios across five dimensions, each of which answers a distinct and critical question about the credit applicant's risk profile.

The first dimension is liquidity: can the applicant meet its short-term obligations? The Current Ratio and Quick Ratio are the primary measures. A Current Ratio consistently above 1.5, with a Quick Ratio that is not dramatically lower, indicates adequate short-term financial flexibility. Below 1.2 on the Current Ratio warrants heightened scrutiny; below 1.0 is a serious concern that should trigger either a request for additional collateral or a refusal of unsecured credit.

The second dimension is leverage: how much debt is the applicant already carrying? The Debt-to-Equity Ratio and Total Debt to Total Assets Ratio reveal the extent of leverage. Heavily leveraged applicants — those with D/E ratios significantly above 2.0 in most industries — represent elevated risk because their financial cushion against revenue disruption is thin. Their capacity to take on additional credit obligations without tipping into distress is correspondingly limited.

The third dimension is debt serviceability: can the applicant afford its existing financing costs? The Interest Coverage Ratio is the primary measure. An Interest Coverage Ratio above 3.0 indicates comfortable debt serviceability; below 2.0 signals that the applicant is already under meaningful financing pressure and has limited capacity to absorb additional obligations.

The fourth dimension is profitability: is the underlying business model generating sustainable returns? Net Profit Margin and Return on Assets are the key indicators. A business with consistent positive margins and adequate returns on its asset base has the earnings capacity to service its obligations over time. Chronic losses or declining margins signal a business model that may not be viable without fundamental change.

The fifth dimension is operational efficiency: how effectively is the business converting its assets into revenue? Asset Turnover and Receivables Turnover reveal whether the business is managing its working capital effectively. Slow receivables turnover, in particular, suggests cash flow pressure that may not be visible in the income statement but will affect the applicant's ability to meet payment obligations consistently.

Individual Financial Ratios provide valuable insights, but a structured scorecard approach — assigning weighted scores to each ratio dimension and aggregating them into an overall credit risk rating — delivers consistency, comparability, and defensibility that judgmental assessment alone cannot match.

A typical credit scorecard might assign the highest weight to liquidity and debt serviceability, reflecting their direct relevance to payment behaviour, with secondary weight on leverage and profitability. The resulting score maps to a credit tier that determines the maximum credit limit, payment terms, and any collateral or guarantee requirements appropriate for the applicant. This structured approach ensures that credit decisions are calibrated to assessed risk rather than commercial optimism or relationship bias.

For credit underwriters assessing external customers or trading partners, a Business Information Report provides an efficient and reliable source of the Financial Ratios and supporting data needed to apply this framework. Rather than gathering and calculating ratio data independently from raw financial statements, underwriters can access pre-calculated ratios alongside payment behaviour, litigation history, and a synthesised credit risk score in a single structured document.

This integration of Business Information Reports into the underwriting workflow dramatically reduces the time required for each assessment while improving the breadth and consistency of the analysis. For organisations processing high volumes of credit applications, this efficiency gain is material — allowing underwriting resources to be allocated to the complex cases that genuinely require human judgment rather than spent on data gathering for straightforward assessments.

Effective credit underwriting does not end at the point of initial approval. A customer whose Financial Ratios indicated a strong credit profile at onboarding may deteriorate significantly over time. Implementing periodic re-underwriting for existing credit accounts — annual for standard accounts, more frequent for high-exposure or higher-risk relationships — ensures that credit terms remain appropriate for current risk rather than being calibrated to a profile that may be years out of date.

Financial Ratios, applied within a structured five-dimension framework and supported by the comprehensive data available in Business Information Reports, provide the most reliable foundation for credit underwriting decisions available to businesses and lenders. The framework described here is accessible to credit teams of all sizes and can be implemented with existing data sources. Businesses that adopt it consistently underwrite better portfolios, experience fewer defaults, and build receivables books that perform in line with expectations rather than delivering the costly surprises that uninformed credit decisions so frequently produce.