From Idea to Launch: A Complete Guide to the Mobile App Development Process

Networking |

2026-05-14 04:13:38

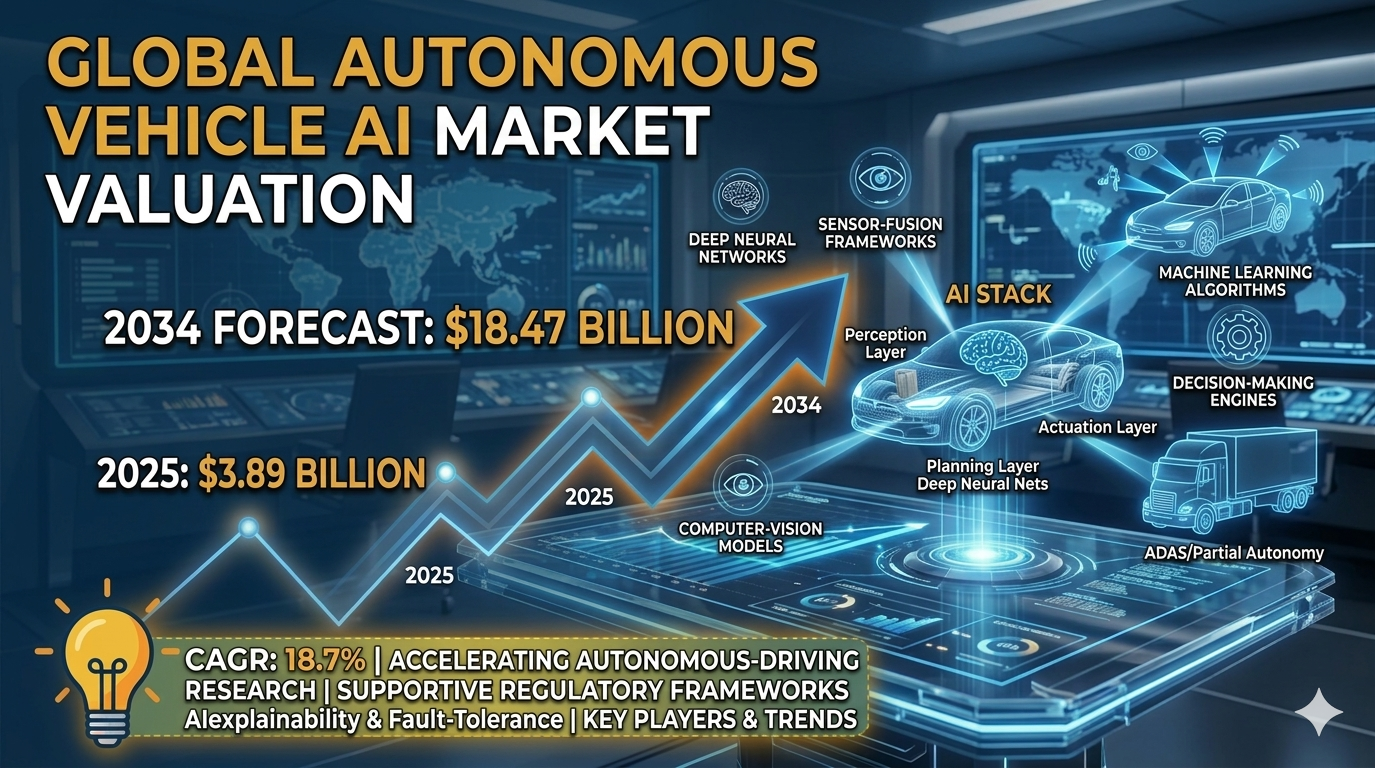

According to a new report from Intel Market Research, the global Autonomous Vehicle AI market was valued at USD 3.89 billion in 2025 and is projected to reach USD 18.47 billion by 2034, exhibiting a robust CAGR of 18.7% during the forecast period (2026–2034). This substantial growth is driven by accelerating investments in autonomous‑driving research, supportive regulatory frameworks, and a rising consumer appetite for safer, more efficient mobility solutions.

Autonomous Vehicle AI refers to the integration of advanced artificial‑intelligence systems that enable vehicles to perceive, interpret, and react to their surroundings without human intervention. The suite of AI‑driven technologies includes machine‑learning algorithms, computer‑vision models, sensor‑fusion frameworks, deep‑neural networks, and decision‑making engines that collectively power real‑time navigation, obstacle detection, path planning, and adaptive control in self‑driving cars.

📥 Download FREE Sample Report:

Autonomous Vehicle AI Market - View in Detailed Research Report

What is Autonomous Vehicle AI?

Autonomous Vehicle AI is the digital brain of a self‑driving car. It merges data from perception sensors-LiDAR, radar, cameras-with high‑precision localization modules (GPS, inertial measurement units) to form a coherent picture of the vehicle’s environment. Prediction engines anticipate the behavior of pedestrians, cyclists, and other road users, while motion‑planning controllers generate safe, efficient trajectories that the vehicle executes through actuation systems. All these components are orchestrated by AI models that are trained on massive, annotated datasets collected from real‑world driving miles.

The market is witnessing exponential growth due to several converging forces. Venture‑capital funding for autonomy startups has surged, while major automakers are allocating multi‑billion‑dollar budgets to integrate AI stacks across new vehicle platforms. Regulatory bodies in North America, Europe, and Asia are progressively defining safety‑certification pathways that recognize AI‑driven functionalities, thereby reducing legal uncertainty and encouraging faster deployments. Smart‑city initiatives and the rollout of 5G connectivity further create an ecosystem where autonomous vehicles can exchange data with infrastructure, unlocking new mobility services.

Key Market Drivers

1. Massive Capital Inflows and Strategic Partnerships

Automotive OEMs, semiconductor firms, and cloud providers are forming joint ventures to co‑develop purpose‑built AI compute platforms. The March 2024 announcement of NVIDIA’s partnership with Mercedes‑Benz to embed the DRIVE Orin AI processor into next‑generation autonomous cars exemplifies how hardware‑software integration accelerates time‑to‑market. Such collaborations reduce development risk and create economies of scale that lower the cost of AI‑enabled vehicle platforms.

2. Advancements in Perception and Decision‑Making Algorithms

High‑definition mapping, deep‑learning‑based object detection, and multi‑modal sensor fusion have dramatically improved safety margins. Modern perception pipelines can resolve objects within 50 ms, enabling real‑time lane‑keeping, obstacle avoidance, and predictive maneuvering. These technical breakthroughs are a core catalyst for broader adoption of autonomous driving solutions across both passenger and commercial fleets.

3. Regulatory Momentum and Safety Standards

Governments worldwide are establishing safety certification pathways that require demonstrable AI explainability and fault‑tolerance. The emergence of standardized testing protocols, along with mandates for over‑the‑air (OTA) update capabilities, reassures regulators and consumers alike, fostering confidence in large‑scale deployments.

Market Challenges

Data Privacy and Security Concerns

Autonomous vehicles generate petabytes of telemetry, video, and lidar data every day. Safeguarding this information while complying with stringent privacy regulations-such as GDPR in Europe and CCPA in California-remains a formidable obstacle for many vendors. Robust encryption, secure‑boot mechanisms, and isolated AI execution environments are essential but add to system complexity and cost.

Standardization Gaps

The absence of unified AI model evaluation criteria hampers cross‑industry collaboration. Divergent testing frameworks lead to duplicated engineering efforts, slower technology roll‑out, and fragmented ecosystems. Industry consortia are actively working on common benchmarks, yet widespread adoption will take time.

Market Restraints

High Capital Expenditure Requirements

Developing, validating, and certifying AI stacks for full‑level autonomy demands substantial R&D spend, sophisticated testing facilities, and extensive sensor suites. These cost barriers limit participation to well‑financed OEMs and technology giants, creating a high entry threshold for newcomers.

Continuous OTA updates also impose long‑term support commitments. Smaller players lacking deep pockets may struggle to sustain the ongoing software lifecycle required for safety‑critical autonomous systems.

Market Opportunities

Growth in Tier‑2 Cities and Emerging Economies

Rapid urbanization in emerging markets is generating demand for shared autonomous mobility solutions. Localized AI models that adapt to regional traffic patterns, road signage, and infrastructure nuances present a sizable growth avenue for technology providers. Partnerships between automotive OEMs and cloud‑AI leaders are unlocking subscription‑based intelligence services that generate recurring revenue streams.

Edge‑Computing and On‑Vehicle Data Management

Edge‑enabled AI processors now handle terabytes of sensor data locally, minimizing reliance on 5G backhaul and preserving privacy. By 2028, fleets are expected to achieve average inference latency below 30 ms, meeting the stringent requirements of city‑scale mobility services. This shift toward decentralized processing supports scalable deployment of autonomous ride‑hailing and logistics fleets.

Regional Market Insights

Segment Analysis

Segment Overview:

|

Segment Category |

Sub‑Segments |

Key Insights |

|

By Type |

|

Decision‑Making Algorithms

|

|

By Application |

|

Full Autonomy (Levels 4‑5)

|

|

By End User |

|

Automotive OEMs

|

|

By Functional Layer |

|

Planning Layer

|

|

By Deployment Scenario |

|

Urban Environments

|

Competitive Landscape

Waymo, the autonomous‑driving subsidiary of Alphabet, remains the clear market leader, leveraging extensive real‑world mileage and a vertically integrated sensor stack. Close behind, Cruise, backed by General Motors, has scaled pilot rides in major U.S. cities and is rapidly expanding its production‑ready robotaxi fleet. Tesla’s Full‑Self‑Driving (FSD) software, embedded in consumer vehicles, creates a hybrid model that blurs the line between driver assistance and full autonomy, granting it a sizable data advantage.

Beyond the headline leaders, a dense ecosystem of specialized players shapes niche segments. Baidu’s Apollo platform supplies open‑source autonomous software to Chinese OEMs, while NVIDIA’s DRIVE platform powers high‑performance AI compute across multiple manufacturers. Mobileye (Intel) continues to refine its camera‑centric perception stack for advanced driver‑assist systems and Level‑4 deployments. Aurora, now a joint venture with Hyundai Motor Group, focuses on a modular autonomy stack for freight and passenger services. Zoox, owned by Amazon, designs purpose‑built robotic taxis with integrated AI. Additional contributors such as Qualcomm, Ford, Honda, and Hyundai Mobis provide critical chipset, sensor, and simulation capabilities that broaden the competitive field and foster rapid innovation.

List of Key Autonomous Vehicle AI Companies Profiled

Report Deliverables

📘 Get Full Report Here:

Autonomous Vehicle AI Market - View Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia‑Pacific: +91 9169164321

🔗 LinkedIn: Follow Us