[ Latest Report ] Olive Market Future Analysis and Market Trends till the forecast period 2032

Other |

2026-03-20 07:17:54

The syngas industry is witnessing strong momentum driven by evolving industrial applications and increasing demand for cleaner fuel alternatives. Recent technological advancements and policy shifts towards sustainability have significantly impacted the syngas market dynamics, resulting in robust business growth and expanded market opportunities globally.

Market Size and Overview

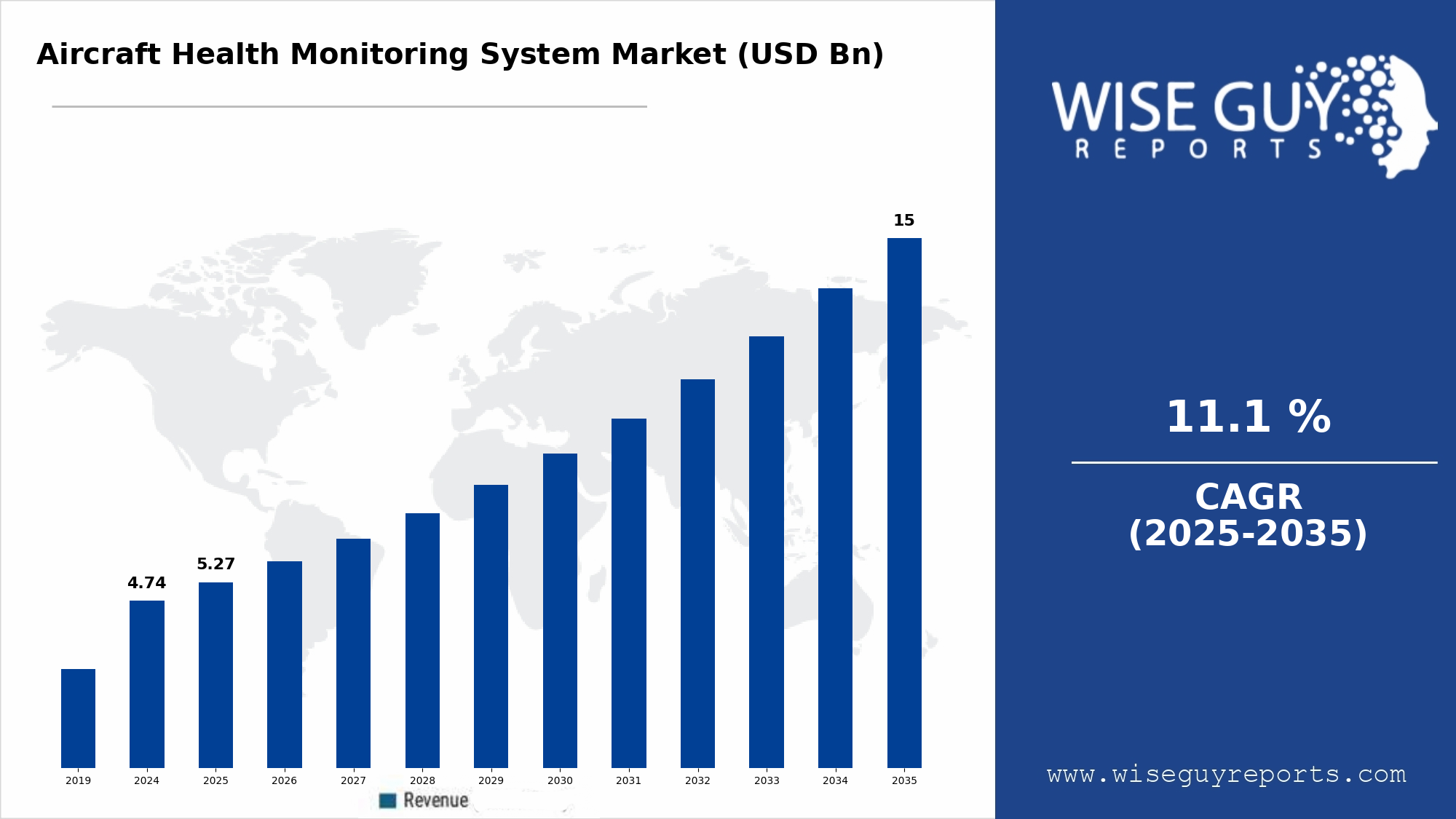

The Global Syngas Market size is estimated to be valued at USD 267.07 Mn Nm³/hr in 2026 and is expected to reach USD 575.80 Mn Nm³/hr by 2033, exhibiting a compound annual growth rate (CAGR) of 11.6% from 2026 to 2033.

Syngas Market Forecast is propelled by increasing syngas application in energy generation and chemical manufacturing processes. The market report highlights that rising adoption of environmentally compliant processes and integration of green hydrogen production are key market drivers contributing to overall market expansion.

Market Segments

The syngas market is segmented broadly into feedstock, technology, and application:

- Feedstock: Coal, natural gas, biomass, and others. Natural gas remains the dominant sub-segment due to its wide availability and lower carbon emissions, while biomass is the fastest-growing segment, with a growth rate of over 13% in 2024-2025 as industries pursue renewable energy options.

- Technology: Coal gasification, steam methane reforming (SMR), and others. SMR dominates with the highest revenue in 2024, supported by enhanced catalyst innovations, whereas biomass gasification is rapidly emerging driven by government incentives for sustainable fuel.

- Application: Power generation, chemicals & fertilizers, transportation fuels, and others. Power generation continues to lead the application landscape, but chemicals and fertilizers show the fastest growth, benefiting from rising demand in agriculture and industrial sectors, backed by strategic investments in Asia-Pacific during 2024.

Market Drivers

One pivotal market driver in 2024 is the global shift towards decarbonization policies. Governments worldwide are encouraging industrial sectors to adopt cleaner technologies such as syngas-based hydrogen production. For instance, in 2024, the European Union allocated over USD 1 billion in grants to support syngas development projects aimed at reducing carbon footprints in the chemical and refining industries. This regulatory support combined with rising environmental awareness has significantly fueled market growth and market revenue expansion.

Segment Analysis

Focusing on the application segment, power generation registered the highest syngas market revenue in 2024, attributed to increasing demand for cleaner electricity and flexible fuel options. The sub-segment of gas turbines utilizing syngas recorded a revenue increase of approximately 15% YoY, as demonstrated by several utility-scale projects in North America. Conversely, the chemicals & fertilizers application is the fastest-growing sub-segment due to new plant installations and favorable raw material supply agreements secured by major industry players in Asia during 2025, further reflecting evolving market opportunities.

Consumer Behaviour Insights

In 2024-2025, buyers and end-users in the syngas market exhibited a growing preference for customizable syngas solutions tailored to specific feedstock types and output requirements. A survey conducted across industrial buyers revealed that 68% prioritized syngas quality and purity based on their production needs, reflecting a shift from standardized to niche solutions. Additionally, pricing sensitivity increased amid fluctuating feedstock costs, leading to demand for flexible contract pricing. Sustainability also emerged as a decisive factor, with 55% of respondents favoring suppliers demonstrating low-carbon footprint technologies, highlighting evolving industry trends.

Key Players

Market leaders influencing the syngas industry include A.H.T Syngas Technology NV, Air Liquide, Air Products and Chemicals Inc., Airpower Technologies Limited, John Wood Group PLC, KBR Inc., Linde Plc, Sasol, Shell Plc, Topsoe AS, Maire Tecnimont Spa, Synthesis Energy Systems Inc., Chiyoda Corporation, Dow Inc., and Methanex Corporation. These market companies have in 2024-2025 executed strategies such as new product deployments (e.g., hydrogen-rich syngas technologies by Linde Plc), capacity expansions (Sasol’s biomass gasification facilities), and regional market entries, significantly impacting market revenue and the syngas market share landscape.

Key Winning Strategies Adopted by Key Players

A key strategy adopted by Shell Plc in 2025 involved integrating carbon capture and storage (CCS) technology directly into their syngas production pipelines, resulting in a 20% reduction in emissions and boosting customer approvals for green syngas contracts. Similarly, KBR Inc. implemented digital twin technologies for process optimization in 2024, enhancing operational efficiency by 18% and supporting predictive maintenance. Lastly, Air Liquide’s adoption of modular syngas plants accelerated deployment times by 30% in emerging markets, enabling them to swiftly capitalize on new market opportunities. These market growth strategies demonstrate impactful approaches beyond traditional expansions.

FAQs

1. Who are the dominant players in the syngas market?

Dominant players include A.H.T Syngas Technology NV, Air Liquide, Air Products and Chemicals Inc., KBR Inc., Shell Plc, and Sasol, all of whom have focused on capacity expansions and technological innovations to enhance market presence.

2. What will be the size of the syngas market in the coming years?

The syngas market is projected to grow from USD 267.07 Mn Nm³/hr in 2026 to approximately USD 575.80 Mn Nm³/hr by 2033, at an 11% CAGR, indicating strong business growth opportunities.

3. Which end-user industry has the largest growth opportunity in the syngas market?

The power generation sector remains dominant in revenue, but chemicals and fertilizers applications present the fastest growth, fueled by expanding agriculture and industrial demand.

4. How will syngas market development trends evolve over the next five years?

Trends indicate heightened adoption of biomass and renewable feedstock-based syngas and integration of digital technologies, supported by regulatory policies encouraging decarbonization and green energy solutions.

5. What is the nature of the competitive landscape and challenges in the syngas market?

The market landscape is competitive with emphasis on innovation and sustainability. Challenges include feedstock price volatility and regulatory compliance, driving players to adopt flexible and green technologies.

6. What go-to-market strategies are commonly adopted in the syngas market?

Key strategies encompass technological advancements like CCS integration, digital twin process optimizations, and modular plant designs for rapid deployment, enhancing operational efficiency and market responsiveness.

Get More Insights on Syngas Market

Get This Report in Japanese Language - 合成ガス市場

Get This Report in Korean Language - 합성가스 시장

Read More Articles Related to this Industry –

Solar Energy: The Future of Clean Energy

Hydrogen Economy: An Eventual Solution For Our Energy And Environment Conservation